The local geography of banking

Despite rapid technological progress and financial innovation, small business banking remains by and large a local affair. Indeed, according to the Italian Banking Association, “the banker’s rule of thumb is to never lend to a client located more than three miles from his office”.11 Many banks comply with this informal “church tower principle” – the idea that they should lend only to firms that can be seen from the local church tower.

If such geographical credit rationing is widely practised, all but the largest firms will depend on the ability and willingness of local banks to lend to them. This also means that local variation in the number and type of bank branches may explain why firms in certain areas are more credit-constrained than similar firms elsewhere.

Read more

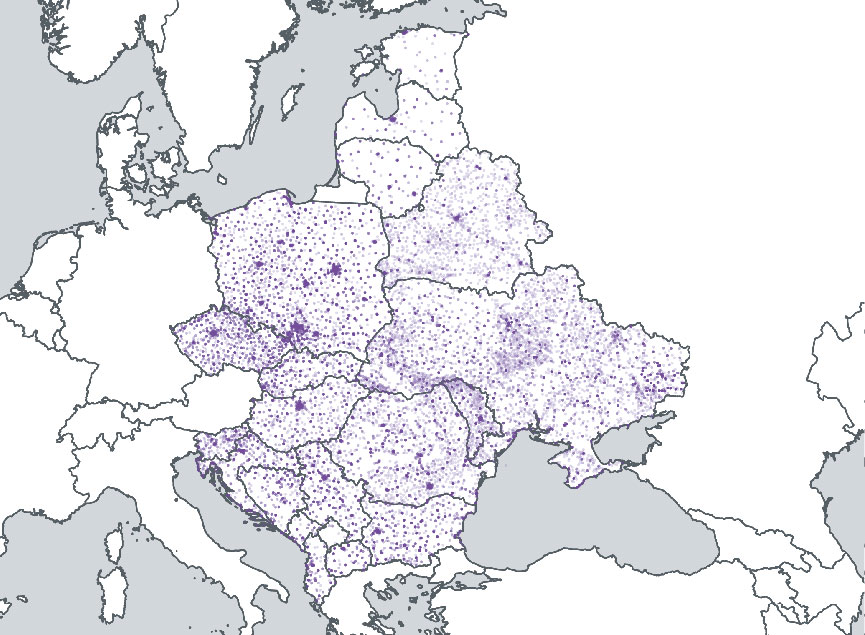

Chart 4.7 depicts the geographical distribution of banking activity across both emerging Europe (see 4.7a) and Russia (see 4.7b). These maps are based on information collected by the EBRD on the geographic coordinates of over 137,786 bank branches. These branches span 1,737 different locations and are owned by over 600 different banks.12 Bank branches are fairly evenly distributed across much of emerging Europe, with greater concentration in capital cities and other urban areas. Russia’s bank branches are concentrated in the south-west of the country, particularly in and around Moscow, as this is where Russia’s economic activity is concentrated.

These detailed branch data are used to construct two indicators for each town or city where BEEPS firms were interviewed. First, the Herfindahl-Hirschman index (HHI) – a measure of market concentration – is calculated for the local area. This HHI index is the sum of the squares of the market shares of the banks in the area, where these market shares are expressed as the share of total branches that is owned by each bank. The index ranges from 0 to 1, with higher values indicating a decrease in competition and an increase in banks’ local market power. The HHI index for emerging Europe as a whole is 0.15, indicating that most local banking markets are only moderately concentrated. Variation across towns and cities is considerable, however.

On the one hand, a concentrated banking market (with a high HHI index) can facilitate long-term lending relationships and thus reduce credit constraints, particularly for more opaque firms. On the other hand, it can also be argued that such concentration may stifle inter-bank competition and thus reduce the supply of credit to firms. While scholars have found evidence for both of these opposing ideas, recent research has tried to reconcile them.

Italian data show, for instance, that while market power (that is to say, higher levels of concentration) can boost firm creation, particularly in opaque industries, at some point the banks’ excessive market power starts to have a negative impact on firm creation. Similarly, cross-country evidence shows that while bank concentration promotes growth in sectors that are dependent on external finance, the overall relationship between bank concentration and economic growth is a negative one.13

The second town/city-level banking indicator that is used in this chapter is the percentage of bank branches that are owned by foreign banks. On average, 39 per cent of the bank branches in a given town or city are foreign-owned. A higher percentage of foreign ownership may reduce small firms’ access to credit if domestic banks possess a comparative advantage in terms of reduced information asymmetries in relation to local firms. This may be because they share a common language and culture or have a better knowledge of local legal and accounting institutions. Such factors may make it easier for domestic banks to base lending decisions on soft data when it comes to smaller local firms, as they have developed long-term relationships with these companies. On the other hand, however, foreign banks may be better at applying transaction technologies that use hard data (such as credit scoring) or collateral-based methods when lending to small businesses. In this case, the presence of foreign banks may actually benefit such firms.

CHART 4.7

Geographical distribution of bank branches across emerging Europe and Russia

(a) Emerging Europe

(b) Russia

Source: BEPS II.

Note: Each dot denotes an individual bank branch.

Step 1: Local banking and credit constraints

Table 4.2 reports the results of statistical analysis explaining the probability of a particular firm being credit-constrained (that is to say, either deciding not to apply for bank credit or being rejected when it applies). Secondary analysis will then use the predictions in this model to determine whether credit-constrained firms innovate less or in a different manner. The first three rows in the table show the main explanatory variables at town/city level: a measure that singles out the most highly concentrated banking markets (those where the HHI index exceeds 0.5); the HHI index in all other towns and cities; and a bank composition indicator that measures the percentage of bank branches in the town/city that are foreign-owned.

Read more

An important assumption in this analysis is that these three local banking variables (or “instruments”) are exogenous in the sense that they only affect firm-level innovation through their impact on the probability of firms being credit-constrained. While plausible, this exclusion restriction could be violated if the location of bank branches is related to local factors that are also correlated with firm-level innovation. While the validity of this assumption cannot be tested directly, there is some evidence to suggest that the concentration and composition of the local banking markets in this dataset are largely exogenous.

First, there is very little correlation between changes in the number of bank branches in a given region between 2002 and 2011 and innovative activity in that region in 2012. Second, the three instruments are not related to firms’ credit demand. Thus, the structure of local credit markets does not appear to have responded in a systematic manner to local demand for external finance on the part of innovative firms. Third, in order to further mitigate endogeneity concerns, (unreported) town/city-level regressions were run where the dependent variable was either “HHI of town/city” or “share of foreign banks”.

This allows us to see the extent to which a battery of town/city-level firm characteristics (and industry fixed effects) can explain local banking structures. If the local banking structure is driven by the composition of the local business sector, we should find significant relationships between firm characteristics (averaged at town/city level) and that banking structure. In this case, there is no significant relationship between, on the one hand, the percentage of small firms, the percentage of large firms, the percentage of sole proprietorships, the percentage of privatised firms, the percentage of exporters or the percentage of audited firms and, on the other hand, bank concentration or the presence of foreign banks. Thus, it appears that the concentration and composition of these banking markets are unrelated to a large set of observable characteristics of the local business sector.

In addition to the three instrumental variables, various other firm and town/city-level characteristics are also included (but not shown for reasons of brevity). This ensures that the analysis carefully controls for other possible determinants of credit constraints. At firm level, these are: the firm’s age and size; whether the firm’s accounts are audited; whether the firm regularly trains its staff; whether it is quality-certified; whether it operates at national level; whether it expects sales to increase; whether it was previously state-owned; and the experience (in years) of the main manager.

At town/city level, these control variables include the size of the relevant town or city and whether that area is the main business centre in the country. They also include the BEEPS V firms’ average responses to questions on: their use of high-speed internet; the frequency of power outages; their assessment of local security, business licensing policies and political instability; and the quality of local courts and the education of the workforce. In addition, they include country and industry fixed effects, so that the analysis effectively compares firms within the same geographical area and within the same industrial sector. This controls for unobservable characteristics common to firms in the same industry or country.

Column 1 shows that a higher HHI index (reflecting a more concentrated local banking market) is associated with a lower probability of a firm being credit-constrained, everything else being equal. In terms of economic magnitude, the coefficient implies that a 1-standard-deviation increase in local bank concentration reduces the probability of a firm being credit-constrained by 5.4 percentage points.

At the same time, however, credit constraints are higher in areas with very concentrated banking markets. This non-linear effect is in line with the literature cited above and shows that while banks’ local market power can help firms to access credit, this only holds up to a certain point. When inter-bank competition declines too much, access to credit starts to suffer.

The U-shaped relationship between local bank concentration and firms’ credit constraints is depicted in Chart 4.8. On the horizontal axis all towns and cities have been allocated to one of five categories with increasing levels of bank concentration. The vertical axis indicates the average percentage of credit-constrained firms in each of those categories. The chart shows that while firms are initially less credit-constrained in more concentrated credit markets (that is to say, those with a higher HHI index), this effect is then reversed once a critical concentration threshold is crossed.

The negative coefficient for the variable “share of foreign banks” in Table 4.2 shows that a higher percentage of foreign-owned bank branches in a firm’s town/city is also associated with less binding credit constraints. Foreign banks may be better placed than domestic banks when it comes to overcoming agency problems and lending to firms. This effect is fairly substantial. A 1-standard-deviation increase in this variable reduces the probability of a firm being credit-constrained by 5.6 percentage points. This reflects the fact that foreign banks are not disadvantaged relative to domestic banks when lending to small and medium-sized businesses. If anything, their presence in the area has had a positive impact on the ability of firms to access external funding. The negative relationship between the percentage of foreign banks and the intensity of credit constraints is also shown graphically in Chart 4.9.

If the positive impact that local bank concentration has on credit constraints reflects the increased ability of banks to build relationships with firms (as economic theory would suggest), this impact should be stronger for relatively opaque firms, for whom such lending relationships are most important.

Columns 2 to 7 in Table 4.2 provide evidence to support this assertion. These columns show interaction terms between the HHI index and various firm-level characteristics. They show that bank concentration reduces credit constraints particularly strongly for smaller firms (column 2), younger firms (column 3), firms without any quality certification (column 4) and unaudited firms (column 5). Together, these findings suggest that, across the transition region, moderately concentrated credit markets may, to some extent, alleviate credit constraints for opaque businesses.

For instance, column 2 shows that a 1-standard-deviation increase in bank concentration reduces the probability of being credit-constrained by 9.4 percentage points for the smallest firms in the sample. For the average firm the reduction is only 5.4 percentage points. That impact becomes progressively smaller for larger and older firms. When a firm reaches 245 employees or 23 years of age, bank concentration starts to have a negative impact on access to credit, indicating that larger and older firms benefit from inter-bank competition.

Columns 6 and 7 of Table 4.2 explore this idea further. In each column the firm sample is split into two groups. The impact that credit market concentration has on credit constraints is then estimated for each of these groups separately. Column 6 distinguishes between firms in high-tech and low-tech industries. High-tech industries are characterised by larger information asymmetries and more severe agency problems between borrowers and lenders. This reflects both the inherent riskiness of high-tech investments and the fact that in high-tech industries collateral is typically intangible. It is therefore easier for firms in low-tech industries to obtain financing via arm’s-length lending techniques, and this type of lending tends to perform better in less concentrated lending markets. The data support this theory, revealing that the impact that local bank concentration has on credit constraints in high-tech industries is almost twice the size of that seen for low-tech industries.

Next, column 7 distinguishes between industries with high (above median) and low (below median) dependence on external finance. Dependence on external finance is calculated by averaging, for each industry, the percentage of working capital that firms in that industry derive from sources other than internal funds and retained earnings (as reported by firms in the BEEPS V survey). As expected, the data show that the impact of bank concentration is more pronounced in industries that are heavily reliant on external funding.

TABLE 4.2

CHART 4.8

CHART 4.9

Local credit markets and firms’ credit constraints

| Dependent variable: Credit constrained | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

|---|---|---|---|---|---|---|---|

|

Highly concentrated (0/1) |

0.2346*** |

0.2190*** |

0.2286*** |

0.2378*** |

0.2329*** |

0.2315*** |

0.2352*** |

|

(0.0757) |

(0.0759) |

(0.0757) |

(0.0758) |

(0.0758) |

(0.0757) |

(0.0757) |

|

|

HHI of town/city |

-0.2385** |

-0.4624*** |

-0.5990*** |

-0.2961*** |

-0.3063*** |

||

|

(0.0937) |

(0.1257) |

(0.1593) |

(0.0982) |

(0.0986) |

|||

|

Share of foreign banks |

-0.1984*** |

-0.2145*** |

-0.2061*** |

-0.1934*** |

-0.2052*** |

-0.2046*** |

-0.2001*** |

|

(0.0601) |

(0.0605) |

(0.0604) |

(0.0601) |

(0.0601) |

(0.0602) |

(0.0602) |

|

|

HHI of town/city * Log of firm size |

0.0784*** |

||||||

|

(0.0284) |

|||||||

|

HHI of town/city * Log of firm age |

0.1383*** |

||||||

|

(0.0453) |

|||||||

|

HHI of town/city * Quality certification (0/1) |

0.1855** |

||||||

|

(0.0788) |

|||||||

|

HHI of town/city * External audit (0/1) |

0.1752** |

||||||

|

(0.0703) |

|||||||

|

HHI of town/city * Low-tech industry (0/1) |

-0.2150** |

||||||

|

(0.0949) |

|||||||

|

HHI of town/city * High-tech industry (0/1) |

-0.3795*** |

||||||

|

(0.1229) |

|||||||

|

HHI of town/city * Low dependence on external finance (0/1) |

-0.1720* |

||||||

|

(0.1013) |

|||||||

|

HHI of town/city * High dependence on external finance (0/1) |

-0.2634*** |

||||||

|

(0.0969) |

|||||||

|

Inverse Mills ratio |

0.6307*** |

0.6327*** |

0.6157*** |

0.6274*** |

0.6312*** |

0.6362*** |

0.6317*** |

|

(0.0909) |

(0.0910) |

(0.0906) |

(0.0907) |

(0.0910) |

(0.0912) |

(0.0908) |

|

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Firm-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Town/city-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Observations |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

|

F-statistic on instrumental variables |

8.50 |

8.22 |

8.26 |

7.47 |

7.51 |

6.92 |

7.18 |

|

Hansen J-statistic (p-value) |

0.88 |

0.21 |

0.64 |

0.59 |

0.04 |

0.21 |

0.91 |

Source: BEEPS V, BEPS II and BankScope.

Note: This table reports the results of regressions estimating the impact that the composition of local banking markets has on firms’ credit constraints – the first stage of an instrumental variable (IV) estimation. The dependent variable is a dummy which is equal to 1 if the firm is credit-constrained and 0 if not. The inverse Mills ratio in column 1 is derived from an unreported Heckman selection probit model. All regressions include a set of firm-level control variables, industry and country fixed effects, town/city-level controls, firm-level controls and a constant. Firm-level controls include log of firm size, log of firm age, external audit, training, quality certification, national sales, expectations of higher sales, log of manager’s experience and previous state ownership. Town/city-level controls include dummies that control for town/city size, main business centre, and firms’ responses to questions on high-speed internet use, power outages, security, business licensing, political instability, courts and education (all averaged at town/city level). Robust standard errors are shown in parentheses; *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively. The F-statistic on IVs is for the F-test that the instruments are jointly insignificant, while the p-value of the Hansen J-statistic is for the overidentification test that the instruments are valid.

Source: BEEPS V and BEPS II.

Note: This bar chart is based on data for all towns and cities with more than 10 BEEPS firms. The y-axis shows the average percentage of constrained firms in the relevant towns and cities. The bars group together towns and cities in increasing order of bank concentration. Concentration is measured by an HHI index where local market shares are expressed as the number of branches belonging to each bank.

Source: BEEPS V, BEPS II and BankScope.

Note: This chart contains data for all towns and cities with more than 10 BEEPS firms.

Step 2: Credit constraints and firm innovation

Table 4.3 provides estimates of the impact that credit constraints have on firm-level innovation. The main explanatory variable is “credit-constrained”, a binary indicator derived from the initial analysis reported in Table 4.2. The analysis in Table 4.3 also takes account of various non-financial determinants of innovation, as well as industry and country fixed effects. Industry fixed effects are particularly important here, as certain industries may present firms with more innovation opportunities via intra-industry spillovers of knowledge and technology.

The first control variable is firm size, which is measured as the number of full-time employees. Firm size is included because larger companies may benefit more from innovative activities owing to economies of scale. The analysis also includes a binary variable indicating whether the firm has its annual financial statements certified by an external auditor. On average, 31 per cent of all firms in the sample have such audited statements. A third firm-level characteristic is the firm’s age, measured as the number of years since its incorporation. Young firms tend to be less transparent than older ones on account of their limited track record. They often also lack the knowledge and experience that is necessary to innovate.

It is also important to take account of a firm’s intrinsic ability to innovate. Hence, a binary variable is included indicating whether the relevant firm has a formal training programme for its permanent employees. 37 per cent of all firms in the sample have such a programme. Moreover, in order to account for firms’ efficiency, a binary variable is included that indicates whether the firm has an internationally recognised quality certification such as ISO 9000. Around 21 per cent of all firms have such a certification.

While economic literature emphasises the role played by competition in driving the returns derived from new technologies, the sign of that effect remains unclear.14 On the one hand, innovation may decline with competition, as firms derive lower returns from the introduction of new technology. On the other hand, though, competition may also drive down mark-ups, encouraging firms to adopt new products and technologies. This analysis contains a measure of competition – a binary variable (“national sales”) that indicates whether the market for a firm’s product is national, as opposed to local. Almost 35 per cent of all BEEPS firms report that their market is national.

Firms undertaking innovation presumably do so with an eye to expanding production and/or increasing efficiency. Thus, innovation may be a response to the investment opportunities available to a firm. While part of this effect is already captured by industry fixed effects, two additional variables are used to control for investment opportunities at the level of individual firms. First, a binary variable is included that indicates whether the firm expects its sales to increase over the next year. A total of 46 per cent of BEEPS firms have a positive growth outlook.

When this battery of firm and industry-level non-financial determinants of innovation are controlled for, we can see that credit-constrained firms are significantly less likely to innovate (see columns 1 and 2 of Table 4.3). The impact of credit constraints is also considerable. These estimates suggest that a credit-constrained firm is 30 percentage points less likely to carry out product innovation and 33 percentage points less likely to conduct process innovation, relative to an equivalent firm with no credit constraints.

Credit constraints have no discernible impact on “soft” innovation such as marketing or organisational innovation. This probably reflects the fact that the implementation of these types of innovation requires less funding and is therefore less dependent on the local availability of bank credit.

The (unreported) coefficients for the control variables are in line with expectations regarding the non-financial drivers of firm-level innovation. The statistically strongest results indicate that innovative activity is higher among firms that expect sales to increase, have recently invested in fixed assets, operate at national level, have a quality certification, use technology that is licensed by a foreign-owned company and provide regular training for employees.

Another interesting question is whether innovation outcomes vary depending on the type of bank from which a firm borrows.

State-owned banks may act as conduits for government-funded programmes boosting firm-level innovation. They may, to some extent, also act like venture capitalists, as they are able to take on more risk (and longer-term risk) than private banks. In this case, borrowing from a state bank could be associated with higher levels of innovation relative to borrowing from a private domestic bank.

Foreign banks, on the other hand, may facilitate the transfer of know-how from foreign to domestic borrowers, thereby boosting the local adoption of foreign products and processes. However, despite all of this, further (unreported) analysis of the sample of borrowing firms suggests that clients of state and foreign banks do not innovate any more or less than firms borrowing from private domestic banks.

TABLE 4.3

Credit constraints and firm-level innovation

| Dependent variable |

Product innovation |

Process innovation |

Soft innovation |

At least two types of innovation |

At least three types of innovation |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

|

Credit-constrained (0/1)

|

-0.4665** |

-0.5730*** |

-0.4006 |

-0.4252** |

-0.2711 |

|

(0.2046) |

(0.2028) |

(0.3029) |

(0.2027) |

(0.1703) |

|

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Area-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Observations |

4,278 |

4,281 |

4,260 |

4,289 |

4,289 |

Source: BEEPS V, BEPS II and BankScope.

Note: This table reports the results of regressions estimating the impact that credit constraints have on firm-level innovation. This is the second stage of our instrumental variable estimation. “Credit-constrained” is the endogenous variable, instrumented as in column 1 of Table 4.2. The inverse Mills ratio is derived from the probit model in column 1 of Table 4.2 and analogous probit models for the other columns. All regressions include industry and country fixed effects, town/city-level controls and a constant. Robust standard errors are given in parentheses; *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively.

Credit constraints and the nature of firm-level innovation

The preceding sections show that access to credit is associated with substantial increases in firm-level innovation, in the form of both new products and new production processes. This strong correlation continues to hold when controlling for an extensive set of firm and town/city-level characteristics and when correcting for the fact that part of this correlation may, to some extent, reflect “reverse causality”. Thus, the evidence suggests that having better access to bank credit does indeed cause firms to introduce new products and processes.

Read more

But how exactly does the ability to borrow from a bank help firms to become more innovative? Chart 4.10 provides some initial information on this subject, showing that firms change the way they innovate once credit constraints are loosened. The red bars show the breakdown of innovation strategies for credit-constrained firms, whereas the green bars show the breakdown for firms without financial constraints. Overall, the main strategies that firms use to introduce new technologies involve: (i) the exploitation and implementation of their own ideas; (ii) the licensing (or informal imitation) of products and processes developed by other firms (typically competitors); and (iii) the development of new products and the upgrading of production processes in cooperation with suppliers, clients and academic institutions.

When comparing the red and green bars, one key difference is the fact that unconstrained firms appear to find it easier to use (and pay for) external ideas. The percentage of firms that are reliant on their own ideas declines from 55 to 49 per cent in the case of product innovation and from 55 to 46 per cent in the case of process innovation. This decline is mirrored by increases in cooperation with suppliers and – more frequently – the licensing of products and processes developed by other firms. This suggests that access to credit may allow firms to access and implement external know-how more quickly and more easily. It also indicates that bank credit can help to facilitate the spread of technology across firms.

Table 4.4 looks at these issues in more detail, applying a similar statistical framework to Table 4.3. More specifically, the table takes a set of innovation outcomes and looks at whether they are affected by firms’ access to credit.

One striking result is that access to credit allows firms not only to introduce products and processes that are new to the firms themselves, but also to adopt products and processes that are new to the main markets where the firms sell their goods or services. This is particularly true of firms that serve a local market, but somewhat less clear-cut for firms that operate at national level. Access to credit helps firms to introduce technologies that are already available elsewhere in the country (or abroad) but are not yet available in their own local markets.

In line with some of the findings of Chart 4.10, this suggests that easier access to credit may help technologies to spread within countries and across local markets. Thus, policies that reduce credit constraints may have collateral benefits in the form of greater intranational diffusion of technology and a gradual reduction in regional growth disparities.15

Importantly, Table 4.4 also indicates a notable limitation of bank credit. In keeping with some of the arguments that were set out at the start of this chapter, data for the transition region show that there is no correlation between easier access to bank credit and in-house innovation in the form of R&D.

This suggests that while bank credit may help firms to adopt existing products and processes that have been developed elsewhere – technologies that are new to those firms and, in many cases, new to local and even national markets – it does little to boost original R&D by firms.

TABLE 4.4

CHART 4.10

Credit constraints and the nature of firm-level innovation

| Product innovation | Process innovation | R&D and acquisition of external knowledge |

||||||

|---|---|---|---|---|---|---|---|---|

| Dependent variable: |

New to firm’s market |

New to local market |

New to national market |

New to firm’s market |

New to local market |

New to national market |

Spent on external knowledge |

R&D |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|

Credit-constrained (0/1)

|

-0.3807** |

-0.3190* |

-0.2606* |

-0.3529** |

-0.2956** |

-0.1587 |

-0.0649 |

-0.0310 |

|

(0.1801) |

(0.1793) |

(0.1354) |

(0.1535) |

(0.1465) |

(0.1005) |

(0.1275) |

(0.1458) |

|

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Firm-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Town/city-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Inverse Mills ratio |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Observations |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

Source: BEEPS V and BEPS II.

Note: This table reports the results of regressions estimating the impact that credit constraints have on various forms of firm-level innovation. This is the second stage of our instrumental variable estimation; the results of the first stage are reported in column 1 of Table 4.2. “Credit-constrained” is the endogenous variable. The inverse Mills ratio is derived from the probit model in column 1 of Table 4.3 and analogous probit models for the other columns. All regressions include industry and country fixed effects, town/city-level controls and a constant. Robust standard errors are given in parentheses; *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively.

Source: BEEPS V.

Note: These bar charts show the differences between the innovation strategies of firms that are

credit-constrained and firms that are not. *, ** and *** indicate significance at the 10%, 5% and

1% levels respectively.