TRANSITION REPORT 2014 Innovation in Transition

TRANSITION REPORT 2014 Innovation in Transition

Cagatay Bircan is a Research Economist at the EBRD. Prior to joining the EBRD, Cagatay worked as a Fixed Income Strategist and Economist at Bank of America Merrill Lynch. He holds a PhD in Economics from University of Michigan and his main research interests are foreign direct investment, international trade and financial development.

Innovation by firms is an important driver of factor productivity and long-term economic growth around the world.1 As Chapter 1 explains, innovation in technologically developed countries typically entails research and development (R&D) and the invention and subsequent patenting of new products and technologies. In less advanced economies, innovation often involves imitation, with firms adopting existing products and processes and adapting them to local circumstances.2 Such innovation tends to be about catching up with the technological frontier, rather than advancing that frontier.

As firms adopt products and processes that have been developed elsewhere, technologies gradually spread across and within countries. The speed of this process varies greatly from country to country, which can explain up to a quarter of total variation in national income levels.3 Despite the central role that such technological diffusion plays in determining growth outcomes, the mechanisms that underpin the spread of new products and processes remain poorly understood. This chapter focuses on one such mechanism: the impact that funding constraints have on firms’ adoption of technology.

Funding constraints may limit the adoption of technology, as external inventions (which are typically context-specific and involve tacit know-how) are costly to integrate into a firm’s production structure. Firms therefore need sufficient financial resources to properly adapt external technologies, products and processes to their local circumstances. If insufficient funding is available, businesses in emerging markets may be unable to fully exploit the easy option of R&D that has been carried out elsewhere. Such firms remain stuck in low-productivity activities, and this may, at country level, contribute to the persistence of divergent growth patterns around the world.

Exactly how – and how much – external finance helps firms to innovate, be it through R&D or the adoption of existing products and processes, remains a matter of debate. One key problem hampering this discussion is the dearth of firm-level information on these two forms of innovation. The EBRD and World Bank’s fifth Business Environment and Enterprise Performance Survey (BEEPS V) goes some way towards remedying this problem.

The empirical analysis contained in this chapter comprises two closely related assessments. First, detailed data about banking structures in towns and cities across the transition region are used to explain the severity of the credit constraints experienced by individual firms in these areas. Second, information on these credit constraints is then used to explain why certain firms innovate more than others.4

The transition region is an interesting place to explore the relationship between access to finance and firm-level innovation, given that – as in other large emerging markets, such as India and China – firms there continue to be plagued by credit constraints.5 At the same time, these firms also perform poorly when it comes to adopting technology. For instance, in the World Economic Forum’s Global Competitiveness Report 2013-2014, Russia is ranked 126th out of 148 countries in terms of firm-level absorption of technology.6

Much of the transition region continues to be characterised by bank-based financial systems, with only shallow public and private equity markets (see Box 4.1). This raises the question of whether access to bank credit can help firms to innovate in the absence of a meaningful supply of risk capital. Broadly speaking, there are two schools of thought on this issue.7

One group of scholars and practitioners takes a rather pessimistic view and stresses the uncertain nature of innovation – particularly R&D. This makes banks less suitable as financiers for four reasons. First, the assets associated with innovation are often intangible, firm-specific and linked to human capital. They are therefore hard to redeploy elsewhere, which makes them difficult for banks to collateralise. Second, innovative firms typically generate volatile cash flows, at least initially. This does not fit well with the inflexible repayment schedules of most loans. Third, banks may simply lack the skills needed to assess early-stage technologies. Lastly, banks may fear that funding new technologies will erode the value of collateral underlying existing loans (which will mostly represent old technologies). For all of these reasons, banks may be either unwilling or unable to fund innovative firms.

A second school of thought takes a much more optimistic view of the situation. According to this view, one of the core functions of banks is the establishment of long-term relationships with firms, during which loan officers gain a deeper understanding of borrowers. Thus, banks may be well placed to fund innovative firms, as such enduring relationships will allow them to understand the business plans and technology involved.

Moreover, as earlier chapters of this Transition Report stress, firm-level innovation entails more than just R&D. It also involves the adoption of existing products and processes that are new to a particular firm, but not to the wider world. Such imitative innovation is arguably less risky and more in line with the risk appetites of most banks. This is particularly true of banks that have funded specific technologies in the past in partnership with other borrowers. In this case, banks may even act as conduits, facilitating the spread of technology across their borrower base.

Lastly, even without financing innovative projects directly or explicitly, banks can still stimulate firm-level innovation. When banks provide firms with straightforward working capital or short-term loans, this can free up internal resources, which firms can then use to finance innovation. Evidence from a broad range of developed countries suggests that firms generally prefer internal funds to any form of external finance when funding innovation.

The limited evidence that is currently available suggests that access to bank credit may indeed help firms to innovate. Findings from the United States show that the deregulation of inter-state banking, which increased bank competition during the 1970s and the 1980s, boosted firm-level innovation (as measured by the number of patents that were subsequently filed in the states concerned).8

Meanwhile, evidence from Italy (a more bank-based economy) suggests that increases in the density of local bank branches are associated with growth in firm-level innovation. This effect is stronger for smaller firms in sectors that are more dependent on external finance.9 Firms that have longer-term borrowing relationships with their banks are also more likely to innovate. Lastly, earlier evidence from the transition region indicates that self-reported credit constraints can partly explain cross-firm variation in innovative activity.10

This chapter extends that body of evidence in two main ways. First, the latest round of the BEEPS survey, which includes a separate innovation module (see Chapter 1), allows much deeper analysis of the channels through which access to credit may (or may not) affect firm-level innovation. Second, by combining such firm-level data with information on the exact geographical location of bank branches across the transition region, it is possible to see how local variation in the presence of banks affects firms’ ability

to innovate.

The analysis in this chapter comprises two stages. First, new data on the geography of banking in the transition region are used to improve our understanding of why certain firms are more credit-constrained than others. Second, this chapter then looks at the extent to which such credit constraints affect a wide variety of innovation outcomes. Before that, though, it is useful to look in more detail at how we assess whether a particular firm is credit-constrained or not.

An assessment of the impact that bank credit has on firm-level innovation calls for a clear and unambiguous measure of whether firms are credit-constrained or not. The measure used here is created by combining firms’ answers to various BEEPS questions.

First, we need to distinguish between firms that need credit and those that do not, as only the former can be credit-constrained. Firms that need credit can then be divided into those that have applied for a loan and those that have decided not to apply because they expect to be turned down by the bank. Finally, firms that have applied can be divided into those that have been granted a loan and those that have been rejected by the bank. Thus, credit-constrained firms can be defined as those that need credit but have either decided not to apply for a loan or were rejected when they applied.

Applying this methodology to the BEEPS V dataset, 52 per cent of all firms surveyed reported needing a bank loan. Just over half of those – 54 per cent – turned out to be credit-constrained: they either did not apply for credit (although they needed a loan) or were rejected by the bank when they did. There is, however, substantial variation both across and within countries in terms of the percentage of credit-constrained firms (see Chart 4.1). This ranges from just 26 per cent in Slovenia to 76 per cent in Ukraine. In some Russian regions (such as Rostov and St Petersburg) this percentage is higher still.

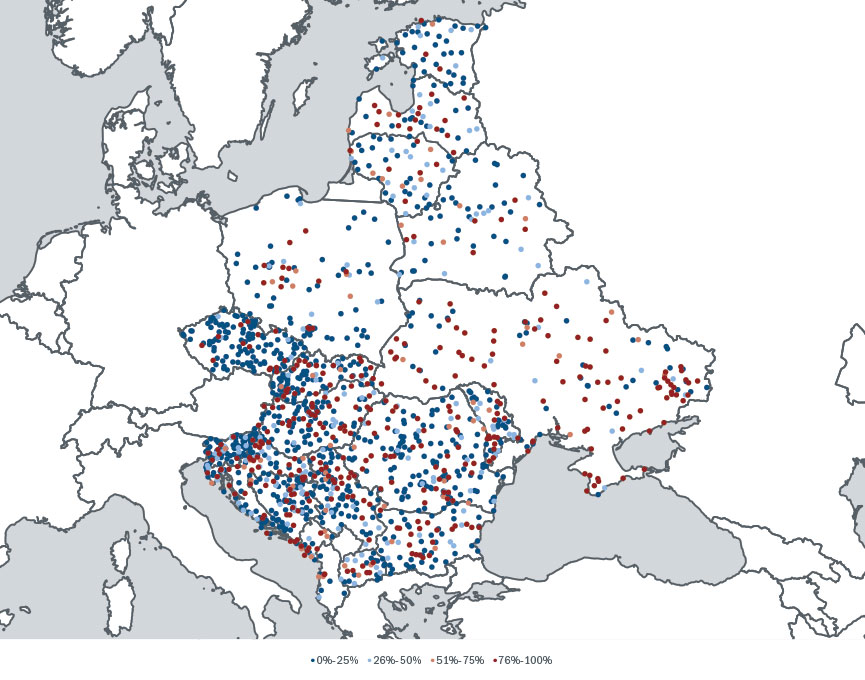

Chart 4.2 provides an even more detailed picture of the regional presence of credit constraints. In this heat map, each dot indicates a town or city where firms were interviewed as part of the BEEPS survey. Red dots indicate areas where a large percentage of firms indicated that they were credit-constrained, whereas blue dots denote areas where only a few firms had problems accessing credit. It is noticeable that there is considerable variation within countries and regions in terms of firms’ ability to successfully attract bank loans. If access to credit affects firms’ ability to innovate, one would expect firms in red areas to have more trouble innovating than firms in blue areas, everything else being equal.

Source: BEEPS V.

Note: Bars indicate the percentage of firms that reported needing a bank loan, but either decided not to apply for one or were rejected when they applied. Blue bars indicate countries, while red bars denote Russian regions.

Source: BEEPS V.

Note: Each dot represents a town or city where firms were interviewed as part of the BEEPS survey. Red colours indicate a higher percentage of credit-constrained firms in that area, while blue colours indicate a lower percentage.

Bank credit and firm-level innovation: a first look Table 4.1 and Chart 4.3 (see p68) take a first look at the relationship between credit constraints and innovation. Firms are grouped into three categories: firms with loans (3,840 firms); firms without loans, but without any need for them (4,723 firms); and firms with no loans and an unfulfilled need for credit (2,762 firms). The third group contains all credit-constrained firms.

Looking at the likelihood of innovative activity, there is a striking difference between the firms with loans and the firms that are credit-constrained. Of the firms with an unmet need for credit, 11.0 per cent, 11.2 per cent and 8.8 per cent have engaged in product innovation, process innovation and R&D respectively over the past three years. When we look at the firms that have been granted loans, these percentages are significantly higher at 15.3, 16.6 and 14.2 per cent respectively. In other words, firms with loans are around 40 per cent more likely to innovate than those without access to credit.

A clear picture – albeit only a preliminary one – is beginning to emerge as regards the relationship between access to credit and innovative activity: firms that innovate tend to be those that apply for a loan and are granted one. Firms that do not demand a loan in the first place are the least likely to innovate, probably because their lack of interest in borrowing coincides with a lack of innovative capacity.

For those firms that have managed to obtain a bank loan – a third of all firms interviewed – Table 4.1 also contains information on the type of bank that lent to them. Only 17 per cent of firms borrowed from a state bank, 29 per cent from a private domestic bank and 54 per cent from a foreign bank. Is innovative activity affected by the type of bank that a firm borrows from?

Table 4.1 suggests not (as does unreported additional analysis). There is some evidence that the clients of state and foreign banks innovate more, but these differences are fairly small and statistically weak, and they disappear when controlling for other firm-level characteristics.

Chart 4.4 shows product and process innovation among credit-constrained and unconstrained firms in selected transition countries. In almost all countries unconstrained firms innovate more than credit-constrained firms.

Chart 4.5 plots data for the same set of countries. Here, the horizontal axis measures the percentage of firms that are credit-constrained, while the vertical axis indicates the difference between the innovative activities of unconstrained and constrained firms. That difference is a rough indicator of the aggregate sensitivity of innovation to firms’ credit constraints in any given country. It indicates the extent to which reducing credit constraints could boost firm-level innovation, given the current economic, political and institutional framework in the country.

The chart shows that in some countries (such as Azerbaijan and Ukraine) credit constraints remain rife among firms. However, in these countries there is also little difference between credit-constrained and unconstrained firms in terms of their innovative behaviour. Consequently, it may be that access to credit has little impact on innovation in these countries, with other constraints – such as an inadequately educated workforce or corruption (see Chapter 3) – having more effect. In contrast, in countries such as Belarus, Lithuania, Romania and Russia, not only are there large numbers of credit-constrained firms but access to bank loans seems to have a relatively large impact in terms of unleashing innovation.

Chart 4.6 indicates that even within countries, at town or city level, there is a strong negative correlation between firms’ credit constraints and innovative activity. The remainder of this chapter looks at this relationship in more detail.

There are two main reasons for conducting this additional analysis. First, a more rigorous investigation is needed to control for other firm-level characteristics, so that the “everything else being equal” condition holds as much as possible. Second, the strong negative correlation between credit constraints and innovation does not necessarily indicate that credit constraints cause a decline in innovation. It could be that causation runs the other way – that is to say, it may be that when firms innovate successfully, banks are more amenable to financing them, thereby reducing credit constraints. One way to address this concern is to consider only credit constraints that are driven by external non-firm-specific factors. To this end, the remainder of this chapter focuses on the impact of credit constraints stemming from exogenous variation in the local banking landscape that surrounds each BEEPS firm.

| Percentage of firms engaged in | ||||

|---|---|---|---|---|

| Product innovation | Process innovation | R&D | Observations | |

| (1) | (2) | (3) | ||

|

Firms with loans |

15.29%*** |

16.62%*** |

14.20%*** |

3,840 |

|

Private domestic bank |

14.20% |

16.65% |

13.48% |

1,120 |

|

State bank |

17.28% |

19.13% |

15.66% |

664 |

|

Foreign bank |

16.09% |

15.68% |

14.79% |

2,056 |

|

Firms without loans |

9.94% |

9.48% |

7.82% |

7,485 |

|

No demand |

9.27% |

8.36% |

7.26% |

4,723 |

|

Credit-constrained |

10.99% |

11.24% |

8.76% |

2,762 |

|

Total |

11.82% |

11.99% |

10.11% |

11,325 |

Source: BEEPS V.

Note: This table reports univariate results on the relationship between access to bank credit and firm-level innovation. *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively for a two-sample t-test for a difference in means with unequal variances. The t-tests compare all firms with loans (top row) with all credit-constrained firms (penultimate row).

Source: BEEPS V.

Note: “No credit needs” denotes firms with no need for bank credit. “Unfulfilled credit needs” denotes firms with a need for bank credit that have either decided not to apply or were rejected when they applied. “Fulfilled credit needs” denotes firms with a need for credit that have received a loan from a bank.

Source: BEEPS V.

Note: Unconstrained firms need loans and are able to borrow from banks. Constrained firms need loans, but either decide not to apply for one or are rejected by the bank when they apply.

Source: BEEPS V.

Note: The vertical axis measures the difference between the average core innovation indices (calculated as the sum of product and process innovation) for unconstrained and constrained firms.

Source: BEEPS V.

Note: Each dot represents a town or city that contains more than 10 BEEPS firms. The x-axis measures the percentage of credit-constrained firms, while the y-axis measures the average core innovation index, which is constructed by regressing the average core innovation observed in the relevant area on the percentage of credit-constrained firms and country fixed effects. The predicted values are then plotted on the y-axis.

Despite rapid technological progress and financial innovation, small business banking remains by and large a local affair. Indeed, according to the Italian Banking Association, “the banker’s rule of thumb is to never lend to a client located more than three miles from his office”.11 Many banks comply with this informal “church tower principle” – the idea that they should lend only to firms that can be seen from the local church tower.

If such geographical credit rationing is widely practised, all but the largest firms will depend on the ability and willingness of local banks to lend to them. This also means that local variation in the number and type of bank branches may explain why firms in certain areas are more credit-constrained than similar firms elsewhere.

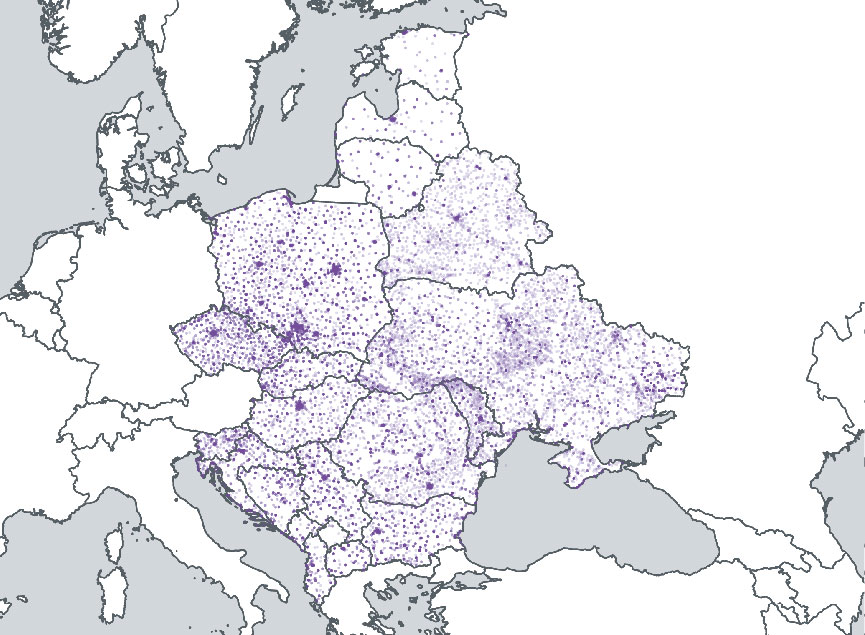

Chart 4.7 depicts the geographical distribution of banking activity across both emerging Europe (see 4.7a) and Russia (see 4.7b). These maps are based on information collected by the EBRD on the geographic coordinates of over 137,786 bank branches. These branches span 1,737 different locations and are owned by over 600 different banks.12 Bank branches are fairly evenly distributed across much of emerging Europe, with greater concentration in capital cities and other urban areas. Russia’s bank branches are concentrated in the south-west of the country, particularly in and around Moscow, as this is where Russia’s economic activity is concentrated.

These detailed branch data are used to construct two indicators for each town or city where BEEPS firms were interviewed. First, the Herfindahl-Hirschman index (HHI) – a measure of market concentration – is calculated for the local area. This HHI index is the sum of the squares of the market shares of the banks in the area, where these market shares are expressed as the share of total branches that is owned by each bank. The index ranges from 0 to 1, with higher values indicating a decrease in competition and an increase in banks’ local market power. The HHI index for emerging Europe as a whole is 0.15, indicating that most local banking markets are only moderately concentrated. Variation across towns and cities is considerable, however.

On the one hand, a concentrated banking market (with a high HHI index) can facilitate long-term lending relationships and thus reduce credit constraints, particularly for more opaque firms. On the other hand, it can also be argued that such concentration may stifle inter-bank competition and thus reduce the supply of credit to firms. While scholars have found evidence for both of these opposing ideas, recent research has tried to reconcile them.

Italian data show, for instance, that while market power (that is to say, higher levels of concentration) can boost firm creation, particularly in opaque industries, at some point the banks’ excessive market power starts to have a negative impact on firm creation. Similarly, cross-country evidence shows that while bank concentration promotes growth in sectors that are dependent on external finance, the overall relationship between bank concentration and economic growth is a negative one.13

The second town/city-level banking indicator that is used in this chapter is the percentage of bank branches that are owned by foreign banks. On average, 39 per cent of the bank branches in a given town or city are foreign-owned. A higher percentage of foreign ownership may reduce small firms’ access to credit if domestic banks possess a comparative advantage in terms of reduced information asymmetries in relation to local firms. This may be because they share a common language and culture or have a better knowledge of local legal and accounting institutions. Such factors may make it easier for domestic banks to base lending decisions on soft data when it comes to smaller local firms, as they have developed long-term relationships with these companies. On the other hand, however, foreign banks may be better at applying transaction technologies that use hard data (such as credit scoring) or collateral-based methods when lending to small businesses. In this case, the presence of foreign banks may actually benefit such firms.

Source: BEPS II.

Note: Each dot denotes an individual bank branch.

Table 4.2 reports the results of statistical analysis explaining the probability of a particular firm being credit-constrained (that is to say, either deciding not to apply for bank credit or being rejected when it applies). Secondary analysis will then use the predictions in this model to determine whether credit-constrained firms innovate less or in a different manner. The first three rows in the table show the main explanatory variables at town/city level: a measure that singles out the most highly concentrated banking markets (those where the HHI index exceeds 0.5); the HHI index in all other towns and cities; and a bank composition indicator that measures the percentage of bank branches in the town/city that are foreign-owned.

An important assumption in this analysis is that these three local banking variables (or “instruments”) are exogenous in the sense that they only affect firm-level innovation through their impact on the probability of firms being credit-constrained. While plausible, this exclusion restriction could be violated if the location of bank branches is related to local factors that are also correlated with firm-level innovation. While the validity of this assumption cannot be tested directly, there is some evidence to suggest that the concentration and composition of the local banking markets in this dataset are largely exogenous.

First, there is very little correlation between changes in the number of bank branches in a given region between 2002 and 2011 and innovative activity in that region in 2012. Second, the three instruments are not related to firms’ credit demand. Thus, the structure of local credit markets does not appear to have responded in a systematic manner to local demand for external finance on the part of innovative firms. Third, in order to further mitigate endogeneity concerns, (unreported) town/city-level regressions were run where the dependent variable was either “HHI of town/city” or “share of foreign banks”.

This allows us to see the extent to which a battery of town/city-level firm characteristics (and industry fixed effects) can explain local banking structures. If the local banking structure is driven by the composition of the local business sector, we should find significant relationships between firm characteristics (averaged at town/city level) and that banking structure. In this case, there is no significant relationship between, on the one hand, the percentage of small firms, the percentage of large firms, the percentage of sole proprietorships, the percentage of privatised firms, the percentage of exporters or the percentage of audited firms and, on the other hand, bank concentration or the presence of foreign banks. Thus, it appears that the concentration and composition of these banking markets are unrelated to a large set of observable characteristics of the local business sector.

In addition to the three instrumental variables, various other firm and town/city-level characteristics are also included (but not shown for reasons of brevity). This ensures that the analysis carefully controls for other possible determinants of credit constraints. At firm level, these are: the firm’s age and size; whether the firm’s accounts are audited; whether the firm regularly trains its staff; whether it is quality-certified; whether it operates at national level; whether it expects sales to increase; whether it was previously state-owned; and the experience (in years) of the main manager.

At town/city level, these control variables include the size of the relevant town or city and whether that area is the main business centre in the country. They also include the BEEPS V firms’ average responses to questions on: their use of high-speed internet; the frequency of power outages; their assessment of local security, business licensing policies and political instability; and the quality of local courts and the education of the workforce. In addition, they include country and industry fixed effects, so that the analysis effectively compares firms within the same geographical area and within the same industrial sector. This controls for unobservable characteristics common to firms in the same industry or country.

Column 1 shows that a higher HHI index (reflecting a more concentrated local banking market) is associated with a lower probability of a firm being credit-constrained, everything else being equal. In terms of economic magnitude, the coefficient implies that a 1-standard-deviation increase in local bank concentration reduces the probability of a firm being credit-constrained by 5.4 percentage points.

At the same time, however, credit constraints are higher in areas with very concentrated banking markets. This non-linear effect is in line with the literature cited above and shows that while banks’ local market power can help firms to access credit, this only holds up to a certain point. When inter-bank competition declines too much, access to credit starts to suffer.

The U-shaped relationship between local bank concentration and firms’ credit constraints is depicted in Chart 4.8. On the horizontal axis all towns and cities have been allocated to one of five categories with increasing levels of bank concentration. The vertical axis indicates the average percentage of credit-constrained firms in each of those categories. The chart shows that while firms are initially less credit-constrained in more concentrated credit markets (that is to say, those with a higher HHI index), this effect is then reversed once a critical concentration threshold is crossed.

The negative coefficient for the variable “share of foreign banks” in Table 4.2 shows that a higher percentage of foreign-owned bank branches in a firm’s town/city is also associated with less binding credit constraints. Foreign banks may be better placed than domestic banks when it comes to overcoming agency problems and lending to firms. This effect is fairly substantial. A 1-standard-deviation increase in this variable reduces the probability of a firm being credit-constrained by 5.6 percentage points. This reflects the fact that foreign banks are not disadvantaged relative to domestic banks when lending to small and medium-sized businesses. If anything, their presence in the area has had a positive impact on the ability of firms to access external funding. The negative relationship between the percentage of foreign banks and the intensity of credit constraints is also shown graphically in Chart 4.9.

If the positive impact that local bank concentration has on credit constraints reflects the increased ability of banks to build relationships with firms (as economic theory would suggest), this impact should be stronger for relatively opaque firms, for whom such lending relationships are most important.

Columns 2 to 7 in Table 4.2 provide evidence to support this assertion. These columns show interaction terms between the HHI index and various firm-level characteristics. They show that bank concentration reduces credit constraints particularly strongly for smaller firms (column 2), younger firms (column 3), firms without any quality certification (column 4) and unaudited firms (column 5). Together, these findings suggest that, across the transition region, moderately concentrated credit markets may, to some extent, alleviate credit constraints for opaque businesses.

For instance, column 2 shows that a 1-standard-deviation increase in bank concentration reduces the probability of being credit-constrained by 9.4 percentage points for the smallest firms in the sample. For the average firm the reduction is only 5.4 percentage points. That impact becomes progressively smaller for larger and older firms. When a firm reaches 245 employees or 23 years of age, bank concentration starts to have a negative impact on access to credit, indicating that larger and older firms benefit from inter-bank competition.

Columns 6 and 7 of Table 4.2 explore this idea further. In each column the firm sample is split into two groups. The impact that credit market concentration has on credit constraints is then estimated for each of these groups separately. Column 6 distinguishes between firms in high-tech and low-tech industries. High-tech industries are characterised by larger information asymmetries and more severe agency problems between borrowers and lenders. This reflects both the inherent riskiness of high-tech investments and the fact that in high-tech industries collateral is typically intangible. It is therefore easier for firms in low-tech industries to obtain financing via arm’s-length lending techniques, and this type of lending tends to perform better in less concentrated lending markets. The data support this theory, revealing that the impact that local bank concentration has on credit constraints in high-tech industries is almost twice the size of that seen for low-tech industries.

Next, column 7 distinguishes between industries with high (above median) and low (below median) dependence on external finance. Dependence on external finance is calculated by averaging, for each industry, the percentage of working capital that firms in that industry derive from sources other than internal funds and retained earnings (as reported by firms in the BEEPS V survey). As expected, the data show that the impact of bank concentration is more pronounced in industries that are heavily reliant on external funding.

| Dependent variable: Credit constrained | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

|---|---|---|---|---|---|---|---|

|

Highly concentrated (0/1) |

0.2346*** |

0.2190*** |

0.2286*** |

0.2378*** |

0.2329*** |

0.2315*** |

0.2352*** |

|

(0.0757) |

(0.0759) |

(0.0757) |

(0.0758) |

(0.0758) |

(0.0757) |

(0.0757) |

|

|

HHI of town/city |

-0.2385** |

-0.4624*** |

-0.5990*** |

-0.2961*** |

-0.3063*** |

||

|

(0.0937) |

(0.1257) |

(0.1593) |

(0.0982) |

(0.0986) |

|||

|

Share of foreign banks |

-0.1984*** |

-0.2145*** |

-0.2061*** |

-0.1934*** |

-0.2052*** |

-0.2046*** |

-0.2001*** |

|

(0.0601) |

(0.0605) |

(0.0604) |

(0.0601) |

(0.0601) |

(0.0602) |

(0.0602) |

|

|

HHI of town/city * Log of firm size |

0.0784*** |

||||||

|

(0.0284) |

|||||||

|

HHI of town/city * Log of firm age |

0.1383*** |

||||||

|

(0.0453) |

|||||||

|

HHI of town/city * Quality certification (0/1) |

0.1855** |

||||||

|

(0.0788) |

|||||||

|

HHI of town/city * External audit (0/1) |

0.1752** |

||||||

|

(0.0703) |

|||||||

|

HHI of town/city * Low-tech industry (0/1) |

-0.2150** |

||||||

|

(0.0949) |

|||||||

|

HHI of town/city * High-tech industry (0/1) |

-0.3795*** |

||||||

|

(0.1229) |

|||||||

|

HHI of town/city * Low dependence on external finance (0/1) |

-0.1720* |

||||||

|

(0.1013) |

|||||||

|

HHI of town/city * High dependence on external finance (0/1) |

-0.2634*** |

||||||

|

(0.0969) |

|||||||

|

Inverse Mills ratio |

0.6307*** |

0.6327*** |

0.6157*** |

0.6274*** |

0.6312*** |

0.6362*** |

0.6317*** |

|

(0.0909) |

(0.0910) |

(0.0906) |

(0.0907) |

(0.0910) |

(0.0912) |

(0.0908) |

|

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Firm-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Town/city-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Observations |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

|

F-statistic on instrumental variables |

8.50 |

8.22 |

8.26 |

7.47 |

7.51 |

6.92 |

7.18 |

|

Hansen J-statistic (p-value) |

0.88 |

0.21 |

0.64 |

0.59 |

0.04 |

0.21 |

0.91 |

Source: BEEPS V, BEPS II and BankScope.

Note: This table reports the results of regressions estimating the impact that the composition of local banking markets has on firms’ credit constraints – the first stage of an instrumental variable (IV) estimation. The dependent variable is a dummy which is equal to 1 if the firm is credit-constrained and 0 if not. The inverse Mills ratio in column 1 is derived from an unreported Heckman selection probit model. All regressions include a set of firm-level control variables, industry and country fixed effects, town/city-level controls, firm-level controls and a constant. Firm-level controls include log of firm size, log of firm age, external audit, training, quality certification, national sales, expectations of higher sales, log of manager’s experience and previous state ownership. Town/city-level controls include dummies that control for town/city size, main business centre, and firms’ responses to questions on high-speed internet use, power outages, security, business licensing, political instability, courts and education (all averaged at town/city level). Robust standard errors are shown in parentheses; *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively. The F-statistic on IVs is for the F-test that the instruments are jointly insignificant, while the p-value of the Hansen J-statistic is for the overidentification test that the instruments are valid.

Source: BEEPS V and BEPS II.

Note: This bar chart is based on data for all towns and cities with more than 10 BEEPS firms. The y-axis shows the average percentage of constrained firms in the relevant towns and cities. The bars group together towns and cities in increasing order of bank concentration. Concentration is measured by an HHI index where local market shares are expressed as the number of branches belonging to each bank.

Source: BEEPS V, BEPS II and BankScope.

Note: This chart contains data for all towns and cities with more than 10 BEEPS firms.

Table 4.3 provides estimates of the impact that credit constraints have on firm-level innovation. The main explanatory variable is “credit-constrained”, a binary indicator derived from the initial analysis reported in Table 4.2. The analysis in Table 4.3 also takes account of various non-financial determinants of innovation, as well as industry and country fixed effects. Industry fixed effects are particularly important here, as certain industries may present firms with more innovation opportunities via intra-industry spillovers of knowledge and technology.

The first control variable is firm size, which is measured as the number of full-time employees. Firm size is included because larger companies may benefit more from innovative activities owing to economies of scale. The analysis also includes a binary variable indicating whether the firm has its annual financial statements certified by an external auditor. On average, 31 per cent of all firms in the sample have such audited statements. A third firm-level characteristic is the firm’s age, measured as the number of years since its incorporation. Young firms tend to be less transparent than older ones on account of their limited track record. They often also lack the knowledge and experience that is necessary to innovate.

It is also important to take account of a firm’s intrinsic ability to innovate. Hence, a binary variable is included indicating whether the relevant firm has a formal training programme for its permanent employees. 37 per cent of all firms in the sample have such a programme. Moreover, in order to account for firms’ efficiency, a binary variable is included that indicates whether the firm has an internationally recognised quality certification such as ISO 9000. Around 21 per cent of all firms have such a certification.

While economic literature emphasises the role played by competition in driving the returns derived from new technologies, the sign of that effect remains unclear.14 On the one hand, innovation may decline with competition, as firms derive lower returns from the introduction of new technology. On the other hand, though, competition may also drive down mark-ups, encouraging firms to adopt new products and technologies. This analysis contains a measure of competition – a binary variable (“national sales”) that indicates whether the market for a firm’s product is national, as opposed to local. Almost 35 per cent of all BEEPS firms report that their market is national.

Firms undertaking innovation presumably do so with an eye to expanding production and/or increasing efficiency. Thus, innovation may be a response to the investment opportunities available to a firm. While part of this effect is already captured by industry fixed effects, two additional variables are used to control for investment opportunities at the level of individual firms. First, a binary variable is included that indicates whether the firm expects its sales to increase over the next year. A total of 46 per cent of BEEPS firms have a positive growth outlook.

When this battery of firm and industry-level non-financial determinants of innovation are controlled for, we can see that credit-constrained firms are significantly less likely to innovate (see columns 1 and 2 of Table 4.3). The impact of credit constraints is also considerable. These estimates suggest that a credit-constrained firm is 30 percentage points less likely to carry out product innovation and 33 percentage points less likely to conduct process innovation, relative to an equivalent firm with no credit constraints.

Credit constraints have no discernible impact on “soft” innovation such as marketing or organisational innovation. This probably reflects the fact that the implementation of these types of innovation requires less funding and is therefore less dependent on the local availability of bank credit.

The (unreported) coefficients for the control variables are in line with expectations regarding the non-financial drivers of firm-level innovation. The statistically strongest results indicate that innovative activity is higher among firms that expect sales to increase, have recently invested in fixed assets, operate at national level, have a quality certification, use technology that is licensed by a foreign-owned company and provide regular training for employees.

Another interesting question is whether innovation outcomes vary depending on the type of bank from which a firm borrows.

State-owned banks may act as conduits for government-funded programmes boosting firm-level innovation. They may, to some extent, also act like venture capitalists, as they are able to take on more risk (and longer-term risk) than private banks. In this case, borrowing from a state bank could be associated with higher levels of innovation relative to borrowing from a private domestic bank.

Foreign banks, on the other hand, may facilitate the transfer of know-how from foreign to domestic borrowers, thereby boosting the local adoption of foreign products and processes. However, despite all of this, further (unreported) analysis of the sample of borrowing firms suggests that clients of state and foreign banks do not innovate any more or less than firms borrowing from private domestic banks.

| Dependent variable |

Product innovation |

Process innovation |

Soft innovation |

At least two types of innovation |

At least three types of innovation |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

|

Credit-constrained (0/1)

|

-0.4665** |

-0.5730*** |

-0.4006 |

-0.4252** |

-0.2711 |

|

(0.2046) |

(0.2028) |

(0.3029) |

(0.2027) |

(0.1703) |

|

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Area-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Observations |

4,278 |

4,281 |

4,260 |

4,289 |

4,289 |

Source: BEEPS V, BEPS II and BankScope.

Note: This table reports the results of regressions estimating the impact that credit constraints have on firm-level innovation. This is the second stage of our instrumental variable estimation. “Credit-constrained” is the endogenous variable, instrumented as in column 1 of Table 4.2. The inverse Mills ratio is derived from the probit model in column 1 of Table 4.2 and analogous probit models for the other columns. All regressions include industry and country fixed effects, town/city-level controls and a constant. Robust standard errors are given in parentheses; *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively.

The preceding sections show that access to credit is associated with substantial increases in firm-level innovation, in the form of both new products and new production processes. This strong correlation continues to hold when controlling for an extensive set of firm and town/city-level characteristics and when correcting for the fact that part of this correlation may, to some extent, reflect “reverse causality”. Thus, the evidence suggests that having better access to bank credit does indeed cause firms to introduce new products and processes.

But how exactly does the ability to borrow from a bank help firms to become more innovative? Chart 4.10 provides some initial information on this subject, showing that firms change the way they innovate once credit constraints are loosened. The red bars show the breakdown of innovation strategies for credit-constrained firms, whereas the green bars show the breakdown for firms without financial constraints. Overall, the main strategies that firms use to introduce new technologies involve: (i) the exploitation and implementation of their own ideas; (ii) the licensing (or informal imitation) of products and processes developed by other firms (typically competitors); and (iii) the development of new products and the upgrading of production processes in cooperation with suppliers, clients and academic institutions.

When comparing the red and green bars, one key difference is the fact that unconstrained firms appear to find it easier to use (and pay for) external ideas. The percentage of firms that are reliant on their own ideas declines from 55 to 49 per cent in the case of product innovation and from 55 to 46 per cent in the case of process innovation. This decline is mirrored by increases in cooperation with suppliers and – more frequently – the licensing of products and processes developed by other firms. This suggests that access to credit may allow firms to access and implement external know-how more quickly and more easily. It also indicates that bank credit can help to facilitate the spread of technology across firms.

Table 4.4 looks at these issues in more detail, applying a similar statistical framework to Table 4.3. More specifically, the table takes a set of innovation outcomes and looks at whether they are affected by firms’ access to credit.

One striking result is that access to credit allows firms not only to introduce products and processes that are new to the firms themselves, but also to adopt products and processes that are new to the main markets where the firms sell their goods or services. This is particularly true of firms that serve a local market, but somewhat less clear-cut for firms that operate at national level. Access to credit helps firms to introduce technologies that are already available elsewhere in the country (or abroad) but are not yet available in their own local markets.

In line with some of the findings of Chart 4.10, this suggests that easier access to credit may help technologies to spread within countries and across local markets. Thus, policies that reduce credit constraints may have collateral benefits in the form of greater intranational diffusion of technology and a gradual reduction in regional growth disparities.15

Importantly, Table 4.4 also indicates a notable limitation of bank credit. In keeping with some of the arguments that were set out at the start of this chapter, data for the transition region show that there is no correlation between easier access to bank credit and in-house innovation in the form of R&D.

This suggests that while bank credit may help firms to adopt existing products and processes that have been developed elsewhere – technologies that are new to those firms and, in many cases, new to local and even national markets – it does little to boost original R&D by firms.

| Product innovation | Process innovation | R&D and acquisition of external knowledge |

||||||

|---|---|---|---|---|---|---|---|---|

| Dependent variable: |

New to firm’s market |

New to local market |

New to national market |

New to firm’s market |

New to local market |

New to national market |

Spent on external knowledge |

R&D |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|

Credit-constrained (0/1)

|

-0.3807** |

-0.3190* |

-0.2606* |

-0.3529** |

-0.2956** |

-0.1587 |

-0.0649 |

-0.0310 |

|

(0.1801) |

(0.1793) |

(0.1354) |

(0.1535) |

(0.1465) |

(0.1005) |

(0.1275) |

(0.1458) |

|

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Firm-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Town/city-level controls |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Inverse Mills ratio |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

Observations |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

4,289 |

Source: BEEPS V and BEPS II.

Note: This table reports the results of regressions estimating the impact that credit constraints have on various forms of firm-level innovation. This is the second stage of our instrumental variable estimation; the results of the first stage are reported in column 1 of Table 4.2. “Credit-constrained” is the endogenous variable. The inverse Mills ratio is derived from the probit model in column 1 of Table 4.3 and analogous probit models for the other columns. All regressions include industry and country fixed effects, town/city-level controls and a constant. Robust standard errors are given in parentheses; *, ** and *** indicate significance at the 10%, 5% and 1% levels respectively.

Source: BEEPS V.

Note: These bar charts show the differences between the innovation strategies of firms that are

credit-constrained and firms that are not. *, ** and *** indicate significance at the 10%, 5% and

1% levels respectively.

The process of firms’ adoption of technology is neither inevitable nor automatic.16 Firms can remain stuck in a pattern of low productivity and weak growth for a long time, even after other businesses in the country have managed to upgrade their operations and move closer to the international technological frontier. Chapter 3 of this Transition Report outlined the main country-level barriers that are currently preventing firms across the EBRD region from benefiting from the world’s technological advances.

This chapter has focused on one key determinant of technological progress at firm level: the ability of entrepreneurs to successfully tap into external funding sources. This analysis shows that while access to bank credit does not matter much for firms’ capacity to conduct in-house R&D – for which access to private or public equity may be necessary (see Box 4.1) – it does determine the pace at which firms can upgrade their production processes, as well as the products and services they offer.

Thus, improving access to bank credit may allow firms in emerging markets to more effectively exploit the global pool of available technologies, increasing the productivity of these firms and helping these countries to catch up with more advanced economies.

Against this background, it is worrying that roughly a quarter of all firms that were interviewed for the BEEPS V survey

indicated that they needed bank credit but were unable to access it. These firms either decided not to apply for a loan for fear of rejection or were refused one when they actually approached a bank.

Of course, not all the businesses will have been creditworthy, and banks may have been right not to lend to them. However, the findings presented in this chapter also indicate that factors external to firms (and thus external to their creditworthiness) are equally important for access to credit. In particular, the probability of a firm managing to access bank credit continues to be strongly influenced by the number and type of banks that happen to be in its immediate vicinity.

This raises the question of what policy-makers in the EBRD region can do to improve access to credit for small businesses. This question has become even more acute in the wake of the global financial crisis, which has had a particularly strong impact on smaller firms,17 thus potentially delaying the economic recovery in many parts of the world.

Moreover, this chapter shows that, in addition to negative cyclical effects, the inability of firms to access bank credit may also have longer-term implications for growth, as credit-constrained firms will find it difficult to upgrade their products and production processes.

While short-term policy responses, such as special funding schemes for small firms, may have a role to play in alleviating such firms’ funding constraints, they are unlikely to solve all problems in the long run. Instead, some banks – at least, those that target smaller businesses – may also need to adjust their lending models at the margins.

Recent research suggests that banks which engage in relationship lending – whereby banks develop long-term lending relationships with small and medium-sized firms, accumulating inside information about these companies – may be better able to lend to relatively opaque borrowers.18 This is particularly true during cyclical downturns, when loan officers tend to be less able to rely on collateral and hard information and need, instead, to conduct an in-depth assessment of a firm’s prospects. This requires more subtle judgements and better information about the abilities and determination of firms’ owners and management. Relationship lenders tend to be better equipped to arrive at such judgements during an economic downturn.

Banks may also need to refine their business models in other ways. For example, financial innovation may contribute to gradual improvements in small firms’ access to financing (see Box 4.2). Lastly, policy-makers can also help banks lend to smaller businesses by establishing credit bureaus and registries, which facilitate the sharing of borrower information among lenders.

Most innovative technologies and products have two things in common. First, they take many years to develop and have unpredictable returns, making them risky investments. Second, they are often introduced by start-ups and younger companies.19 These characteristics mean that bank credit – and debt more generally – is not an ideal funding instrument for R&D, as this chapter demonstrates.

Instead, advanced economies have traditionally used equity to finance innovative companies. Private equity (PE) and venture capital (VC) funds provide equity to a diverse portfolio of companies, as well as offering know-how and incentives to help them realise their potential.

There is now growing evidence from both Europe and the United States that companies backed by PE or VC carry out more patented innovations and have their patents cited more often (an indication of the quality of these innovations).20 This is not simply because PE/VC funds are good at picking the most promising companies and sectors. It also reflects the fact that these funds add economic value to companies in their portfolios through improvements in corporate governance, better monitoring of managers and superior access to human capital.21

While smaller and younger companies stand to gain the most from such professional expertise, equity financing can also benefit more established businesses. Without adequate modernisation or R&D, older and larger companies may find it hard to maintain brand names or introduce new products or processes. As a result, their growth may stagnate.

This is especially relevant for larger and older firms in the transition region that need to catch up with the technological frontier in terms of corporate governance and the sophistication of products. For these more established companies, equity financing may not only boost R&D, but also help them to catch up by adopting products and processes from elsewhere.

Unfortunately, over the past decade the transition region has seen only modest levels of PE/VC financing, which has tended to remain focused on the United States and western Europe. While equity funding is increasingly being directed towards emerging markets, the region has also lagged behind Brazil, China, India and South Africa when it comes to securing such funding.

Chart 4.1.1 shows, on the left-hand axis, the average number of private equity deals in each EBRD subregion (4.1.1a), comparing those figures with other emerging economies and the United Kingdom (4.1.1b). The CEB region and Russia stand out as having the highest number of deals in the transition region, which secures investment in a total of around 190 companies a year on average. However, this figure pales in comparison with Brazil, China, India and South Africa. The transition region also lags far behind the United Kingdom, where upwards of 600 companies typically attract equity investment in any given year.

Emerging markets have become more attractive for private equity investors over the past decade, but the impact of the global recession of 2009 has varied from country to country. The average number of private equity deals has risen considerably in Russia and Turkey, while the CEB, SEMED and SEE regions have all seen declines in the post-crisis period. This partly reflects the impact of bank deleveraging in Europe, with the United Kingdom also seeing fewer deals in this period. However, Brazil, China, India and South Africa are continuing to see strong growth in such deals.

Chart 4.1.1 also shows, on the right-hand axis, the penetration ratio for private-equity investment in the various EBRD regions (4.1.1a) and the same group of comparator countries (4.1.1b). The chart shows that in some of the largest transition countries, such as Russia and Turkey, PE/VC flows barely constitute 0.05 per cent of GDP, while that penetration ratio is typically upwards of 0.25 per cent in more mature markets. PE/VC penetration in the CEB region compares favourably with mature markets, despite a sizeable decline since 2008. The SEE region has also suffered a particularly strong decline in PE/VC penetration. Overall, then, the contribution that PE/VC investment makes to innovative activity may well remain limited in most of the EBRD region.

Why has private equity financing been so lacklustre in the region? Table 4.1.1 offers a few clues using an index that measures countries’ attractiveness for venture capital and private equity.22 The table contains details of six different indicators measuring how far each country is from the United States in terms of its attractiveness for equity financing.

Panel A shows the transition region and Panel B shows a set of comparator countries. The table shows that the development of capital markets is a significant area in this regard – one in which the transition region is a long way from catching up with the major emerging economies and more developed economies. The lack of developed stock markets, the paucity of opportunities for initial public offerings and mergers and acquisitions, and the immature credit markets all serve to discourage PE/VC funds, for which viable exit strategies are crucial in order to realise financial returns. The region also scores less favourably in terms of its human and social environment, indicating that it does not have sufficient human capital to attract PE/VC investors. In addition, there is room for improvement both in terms of the ease of doing business and corporate R&D spending (in order to boost entrepreneurial opportunities) and in terms of investor protection and corporate governance rules. On a more positive note, the region’s taxation system compares favourably with developed economies.

| CEB | SEE | Turkey | EEC | Russia | Central Asia | SEMED |

| Brazil, China, India and South Africa | United Kingdom |

Source: Thomson Reuters VentureXpert, July 2014.

Note: The left-hand axis measures the average number of portfolio companies receiving private equity financing per year. The right-hand axis measures the average private equity penetration rate – that is to say, average annual private equity investment as a percentage of current GDP.

Panel A

| Country | Ranking | Index | Economic activity |

Capital markets |

Taxation | Investor protection and corporate governance |

Human and social environment |

Entrepreneurial opportunities |

|---|---|---|---|---|---|---|---|---|

|

Poland |

29 |

69.9 |

81.2 |

70.0 |

101.3 |

69.5 |

61.5 |

64.0 |

|

Turkey |

30 |

69.7 |

90.2 |

75.2 |

109.4 |

67.4 |

51.0 |

60.5 |

|

Russia |

41 |

63.0 |

91.7 |

72.1 |

100.7 |

46.5 |

33.6 |

66.5 |

|

Lithuania |

43 |

61.0 |

68.9 |

47.1 |

103.2 |

74.5 |

65.2 |

62.7 |

|

Hungary |

45 |

58.8 |

72.8 |

45.6 |

96.5 |

63.6 |

64.3 |

60.5 |

|

Slovak Rep. |

48 |

56.8 |

66.6 |

48.7 |

94.2 |

59.3 |

54.2 |

57.7 |

|

Morocco |

49 |

55.2 |

81.1 |

51.3 |

108.2 |

60.3 |

38.5 |

50.1 |

|

Slovenia |

50 |

54.5 |

59.5 |

33.3 |

112.1 |

68.0 |

70.4 |

66.8 |

|

Estonia |

51 |

54.2 |

62.1 |

31.4 |

109.2 |

85.2 |

61.6 |

65.9 |

|

Romania |

52 |

53.9 |

83.2 |

42.4 |

83.1 |

58.7 |

42.4 |

58.6 |

|

Jordan |

53 |

53.5 |

66.4 |

45.9 |

95.4 |

47.9 |

58.6 |

52.4 |

|

Latvia |

55 |

53.2 |

68.3 |

32.0 |

107.2 |

77.7 |

58.7 |

61.1 |

|

Bulgaria |

56 |

53.2 |

63.5 |

40.6 |

89.1 |

55.4 |

62.1 |

55.9 |

|

Tunisia |

60 |

50.3 |

64.1 |

44.1 |

109.2 |

63.7 |

50.9 |

38.6 |

|

Ukraine |

63 |

48.0 |

72.8 |

49.2 |

82.7 |

43.3 |

27.0 |

48.7 |

|

Croatia |

64 |

47.6 |

60.3 |

34.1 |

108.1 |

53.6 |

41.3 |

56.8 |

|

Egypt |

69 |

46.4 |

76.6 |

49.3 |

83.0 |

46.6 |

19.8 |

46.7 |

|

Kazakhstan |

70 |

45.9 |

90.4 |

23.9 |

98.2 |

64.5 |

42.1 |

56.5 |

|

Georgia |

71 |

45.9 |

57.5 |

27.3 |

104.7 |

61.7 |

58.8 |

50.7 |

|

Bosnia and Herz. |

75 |

43.6 |

42.5 |

31.0 |

74.5 |

52.6 |

53.0 |

50.7 |

|

FYR Macedonia |

78 |

42.9 |

36.6 |

25.3 |

93.8 |

67.0 |

59.9 |

53.2 |

|

Serbia |

79 |

42.8 |

55.9 |

26.7 |

44.8 |

47.7 |

57.8 |

55.0 |

|

Montenegro |

84 |

38.8 |

35.1 |

20.5 |

86.6 |

71.0 |

74.9 |

40.2 |

|

Armenia |

86 |

38.6 |

52.0 |

16.8 |

94.4 |

66.8 |

46.0 |

55.8 |

|

Mongolia |

87 |

38.3 |

72.3 |

18.7 |

73.6 |

55.8 |

40.6 |

48.5 |

|

Belarus |

92 |

33.1 |

78.5 |

12.0 |

93.8 |

35.2 |

44.2 |

53.6 |

|

Moldova |

96 |

29.0 |

56.1 |

11.4 |

93.2 |

54.1 |

26.2 |

41.4 |

|

Kyrgyz Rep. |

101 |

25.4 |

58.2 |

10.5 |

66.5 |

45.0 |

23.2 |

33.1 |

|

Albania |

106 |

23.4 |

54.5 |

5.0 |

74.9 |

57.7 |

37.6 |

42.7 |

Panel B

| Country | Ranking | Index | Economic activity | Capital markets | Taxation | Investor protection and corporate governance |

Human and social environment |

Entrepreneurial opportunities |

|---|---|---|---|---|---|---|---|---|

|

United States |

1 |

100.0 |

100.0 |

100.0 |

100.0 |

100.0 |

100.0 |

100.0 |

|

United Kingdom |

4 |

95.3 |

92.2 |

87.2 |

122.6 |

107.9 |

103.4 |

92.4 |

|

China |

22 |

78.4 |

116.5 |

86.0 |

109.6 |

62.6 |

53.1 |

73.4 |

|

India |

28 |

70.7 |

94.5 |

81.4 |

84.7 |

66.0 |

49.2 |

60.8 |

|

South Africa |

32 |

69.4 |

62.3 |

76.8 |

111.3 |

87.1 |

43.6 |

67.4 |

|

Brazil |

40 |

64.0 |

94.7 |

77.3 |

23.0 |

58.0 |

55.1 |

55.5 |

Source: 2014 Venture Capital and Private Equity Country Attractiveness Index.

Note: The Venture Capital and Private Equity Country Attractiveness Index measures the attractiveness of a country for investors in limited partnerships on the basis of six key drivers: economic activity (size of the economy, GDP growth and unemployment); capital markets (size and liquidity of stock markets, IPO and M&A activity, credit markets and sophistication of financial markets); taxation (entrepreneurial tax incentives and administrative burdens); investor protection (quality of corporate governance, security of property rights and quality of legal enforcement); human and social environment (human capital, labour market policies and crime); and entrepreneurial opportunities (innovation capacity, ease of doing business and corporate R&D). The United States is used as a benchmark, with values equal to 100; lower values indicate lower levels of attractiveness. Azerbaijan, Kosovo, Tajikistan, Turkmenistan and Uzbekistan are not covered.

Firm-level innovation – and private-sector dynamism more generally – may pose challenges to banks and other financial intermediaries that need to decide which entrepreneurs deserve funding and which do not. The more quickly technologies evolve, the more difficult it is for banks to distinguish between creditworthy loan applicants and firms that are too risky.

To some extent, this is simply because business plans that involve new and untested products or processes are more difficult to evaluate. It may also be complicated to value collateral that involves new technologies. Consequently, if they are to continue lending to innovative firms, banks will have to constantly update their screening processes. Thus, banks themselves will need to innovate if they are to continue facilitating firm-level innovation.23

Across the transition region, various forms of financial innovation are currently helping banks and other financial service providers to continue lending to a broad spectrum of clients.

Factoring: Factoring involves the sale of accounts receivable, at a discount, to a specialist lender. This is an important source of external financing for small and medium-sized enterprises (SMEs) around the world. Total global turnover from factoring stood at €2.2 trillion in 2013 and has been growing at an average annual rate of 15 per cent in the wake of the global financial crisis. This suggests that factoring has acted as a substitute for traditional bank lending in the tight credit environment currently faced by SMEs. An important innovation in the area of factoring has been the emergence of invoice-trading platforms. These platforms enable SMEs to auction off their receivables to a broader range of institutional investors with greater flexibility. This helps firms to gain access to more cost-efficient working capital. Following the success of the US-based Receivables Exchange, a number of similar start-ups have emerged in other countries. Slovenia’s Borza Terjatev is the first online receivables exchange in the EBRD region.

Credit scoring: Banks use credit scoring to automatically process information on a small number of standard characteristics of borrowers in order to predict the credit risk associated with each borrower. This was originally used for consumer and mortgage lending, but in the 1990s it began to be used for small business loans as well, after Fair, Isaac and Company developed a credit-scoring model for SME lending in the United States. Today, over 90 per cent of US small business lenders use this technique. Across the transition region, more and more banks and microfinance institutions are introducing credit-scoring tools as part of broader improvements in screening and underwriting policies. One particularly interesting example is the recent introduction by various Turkish banks of a credit-scoring tool aimed specifically at farmers and small-scale agricultural firms. This agricultural client assessment programme was developed by the Frankfurt School of Finance & Management to help financial institutions lend to agricultural firms. The innovative credit-scoring tool allows relationship managers and loan officers with limited knowledge of agriculture to process loan applications submitted by farmers and entrepreneurs working in the areas of crop production, dairy production, cattle fattening, apiculture and poultry.

Online lenders: Online financial service providers vary widely – from those that lend to businesses from their own balance sheets (such as the US-based OnDeck or Kabbage) to peer-to-peer (P2P) business lenders (such as the UK-based FundingCircle), which link institutional investors with borrowers and charge a fee for the origination and vetting. These organisations use proprietary credit algorithms to gain a better understanding of small businesses’ financial health and make quick decisions on lending. In the transition region, the first online lenders are only just beginning to emerge. The Estonian company isePankur has gained traction in the area of P2P lending, although it focuses on consumer loans, rather than lending to businesses.

“Big data” and alternative data sources: The screening of SMEs is particularly challenging in emerging markets, where credit bureaus often have only patchy coverage, firms’ financial histories are limited and collateral is often unavailable. A number of start-ups are trying to address this issue by leveraging alternative data sources (such as applicants’ online transaction records, mobile phone usage and activity on social networks) to evaluate repayment risk. German company Kreditech, which has offices in Prague, Moscow, Warsaw and Ukraine, sells a credit-scoring tool that is based on “big data” (such as e-commerce transactions). It also underwrites its own consumer loans in a number of countries (including Russia and Poland). Meanwhile, Friendlyscore.com is a Polish start-up that sells lenders credit scorecards that are based on Facebook data.

Psychometric testing: A growing number of financial institutions are assessing business owners’ creditworthiness using computer-based psychometric tests. By asking questions about applicants’ characters, abilities and attitudes, they hope to identify high-potential, low-risk entrepreneurs (who may not have a credit history or collateral). A psychometric test developed by the Entrepreneurial Finance Lab – a spin-off from a Harvard University research project – is currently being applied by various financial institutions across Latin America, Asia and Africa.

D. Acemoğlu, P. Aghion and F. Zilibotti (2006)

“Distance to Frontier, Selection, and Economic Growth”, Journal of the European Economic Association, Vol. 4, pp. 37-74.

V. Acharya, O.F. Gottschalg, M. Hahn and C. Kehoe (2013)

“Corporate Governance and Value Creation: Evidence from Private Equity”, Review of Financial Studies, Vol. 26, No. 2, pp. 368-402.

P. Aghion and P. Howitt (1992)

“A model of growth through creative destruction”, Econometrica, Vol. 60, pp. 323-351.

M.D. Amore, C. Schneider and A. Žaldokas (2013)

“Credit Supply and Corporate Innovation”, Journal of Financial Economics, forthcoming.

T.H.L. Beck, H. Degryse, R. De Haas and N. Van Horen (2014)

“When arms’ length is too far: relationship banking over the business cycle”, EBRD Working Paper No. 169.

L. Benfratello, F. Schiantarelli and A. Sembenelli (2008)

“Banks and Innovation: Microeconometric Evidence on Italian Firms”, Journal of Financial Economics, Vol. 90, No. 2, pp. 197-217.

S. Bernstein, X. Giroud and R. Townsend (2014)

“The Impact of Venture Capital Monitoring: Evidence from a Natural Experiment”, mimeo.

C. Bircan and R. De Haas (2014)

“Banks and Technology Adoption: Firm-Level Evidence from Russia”, EBRD working paper, forthcoming.

P. Bolton, X. Freixas, L. Gambacorta and P.E. Mistrulli (2013)

“Relationship and Transaction Lending in a Crisis”, Bank of Italy Working Paper No. 917.

E. Bonaccorsi di Patti and G. Dell’Ariccia (2004)

“Bank Competition and Firm Creation”, Journal of Money, Credit and Banking, Vol. 36, No. 2, pp. 225-251.

N. Cetorelli and M. Gambera (2001),

“Banking Market Structure, Financial Dependence and Growth: International Evidence from Industry Data”, The Journal of Finance, Vol. 56, No. 2, pp. 617-648.

S. Chava, A. Oettl, A. Subramanian and K.V. Subramanian (2013)

“Banking Deregulation and Innovation”, Journal of Financial Economics, Vol. 109, No. 3, pp. 759-774.

G. Chodorow-Reich (2014)

“The Employment Effects of Credit Market Disruptions: Firm-Level Evidence from the 2008-09 Financial Crisis”, Quarterly Journal of Economics, Vol. 129, No. 1, pp. 1-59.

D. Comin and B. Hobijn (2010)

“An Exploration of Technology Diffusion”, American Economic Review, Vol. 100, No. 5, pp. 2031-59.

F. Cornelli, Z. Kominek and A. Ljungqvist (2013)

“Monitoring Managers: Does It Matter?”, The Journal of Finance, Vol. 68, No. 2, pp. 431-481.

J. Eaton and S. Kortum (1999)

“International Patenting and Technology Diffusion: Theory and Measurement”, International Economic Review, Vol. 40, pp. 537-570.

Y. Gorodnichenko and M. Schnitzer (2013)

“Financial Constraints and Innovation: Why Poor Countries Don’t Catch Up”, Journal of the European Economic Association, Vol. 11, pp. 1115-1152.

L. Guiso, P. Sapienza and L. Zingales (2004)

“Does Local Financial Development Matter?”, Quarterly Journal of Economics, Vol. 119, pp. 929-969.

S. Guriev and D. Kvasov (2009)

“Imperfect Competition in Financial Markets and Capital Structure”, Journal of Economic Behavior & Organization, Vol. 72, pp. 131-146.

A.M. Herrera and R. Minetti (2007)

“Informed Finance and Technological Change: Evidence from Credit Relationships”, Journal of Financial Economics, Vol. 83, pp. 223-269.

W. Keller (2004)

“International Technology Diffusion”, Journal of Economic Literature, Vol. 42, pp. 752-782.

L. Laeven, R. Levine and S. Michalopolous (2013)

“Financial Innovation and Endogenous Growth”, mimeo.

J. Lerner, M. Sorensen and P. Strömberg (2011)

“Private Equity and Long-Run Investment: The Case of Innovation”, The Journal of Finance, Vol. 66, No. 2, pp. 445-477.

A. Popov and P. Roosenboom (2009)

“Does Private Equity Investment Spur Innovation? Evidence from Europe”, ECB Working Paper No. 1063.

C. Schneider and R. Veugelers (2010)

“On Young Highly Innovative Companies: Why They Matter and How (Not) to Policy Support Them”, Industrial and Corporate Change, Vol. 19, No. 4, pp. 969-1007.