TRANSITION REPORT 2014 Innovation in Transition

TRANSITION REPORT 2014 Innovation in Transition

Helena Schweiger is a Senior Economist at the EBRD. She holds a PhD in Economics from University of Maryland, College Park and her main research interests include applying micro-to-macro empirical analysis to try to understand the causes of differences in productivity and growth across countries, businesses and time, and their policy implications.

At the beginning of the transition process virtually every country in the EBRD region achieved large one-off productivity gains by laying off excess workers, cutting other costs and improving the use of capacity. There remains scope for leveraging such drivers of productivity in those countries that are still at a relatively early stage of the process. In those countries, improving management practices may also have a large positive impact on productivity. In more advanced transition countries, firm-level innovation plays a more important role in boosting firms’ productivity.

This chapter looks at the impact that different forms of innovation and the quality of management practices have on firms’ labour productivity1 (calculated as turnover per worker), using the EBRD and World Bank’s fifth Business Environment and Enterprise Performance Survey (BEEPS V) and the Middle East and North Africa Enterprise Surveys (MENA ES) conducted by the EBRD, the World Bank and the European Investment Bank. It first presents basic information about the labour productivity of firms across the transition region, before investigating the relationship between innovation and productivity and comparing the effect that innovation has on productivity in high and low-tech sectors. The chapter then examines productivity gains stemming from improvements in management practices, comparing them with returns to process innovation in various regions. It concludes by examining the relative export performances of innovative and less innovative industries.

All over the world, large and persistent differences in productivity continue to exist across both firms and countries.2 Transition countries are no exception in this regard. There are firms with low and high productivity in each of these countries: there are highly productive firms in Central Asia and poorly performing firms in the EU. What determines aggregate productivity is the percentage of firms with low productivity relative to the percentage of firms with high productivity. Compared with Israel, an advanced industrialised country with several innovation successes,3 transition countries have a higher percentage of firms with low productivity and a lower percentage of highly productive firms (see Chart 2.1). This, of course, results in lower average productivity at the country level.

Israel also has a more compressed distribution of firm productivity than any of the other countries shown – possibly because Israeli firms tend to be more advanced in terms of the technology they are using, but also because Israel is more competitive than the average transition country.4 The ratio of the 90th to the 10th percentiles of the log of labour productivity – a measure of variation in productivity across firms – ranges from 1.19 in Israel to 1.59 in Tajikistan. In most EBRD countries and regions this ratio tends to be higher for services than it is for manufacturing. Within manufacturing, the productivity spread tends to be lowest in high-tech sectors, which face strong competitive pressure to innovate and reduce costs. The spread is highest among providers of services, which (unlike producers of manufactured goods) do not face such strong competition from imports.

There is evidence that the performance of sectors which produce or are heavily reliant on information and communication technology (ICT) and their ability to innovate and adopt technology are important drivers of cross-country differences in aggregate productivity.5

ICT-intensive sectors are characterised by high levels of labour productivity, and this holds for the transition region as well. The largest productivity premiums for these sectors relative to other manufacturing industries can be found in central Europe and the Baltic states (CEB), south-eastern Europe (SEE), and eastern Europe and the Caucasus (EEC). Within the EEC region, this is particularly true of Armenia and Azerbaijan, two countries with a strong focus on ICT in their innovation policies.6 However, in most countries differences between the productivity levels of individual firms are also large within ICT-intensive sectors. Thus, even in these sectors, it seems that many firms have ample scope for improving their productivity.

Source: BEEPS V, MENA ES and authors’ calculations.

Note: The red line is the fitted distribution for Israel. Firm-level labour productivity is measured in logs and defined as turnover per employee. Cross-country differences in sectoral composition are controlled for. Turnover in local currency is converted to US dollars using the average official exchange rate.7 Density is calculated by dividing the relative frequency (in other words, the number of values that fall into each class, divided by the number of observations in the set) by the width of the class.

Our analysis now turns to the relationship between innovation and the productivity of firms. Policy-makers and researchers widely acknowledge that innovation is essential for increasing productivity.8 However, while a positive correlation between product innovation and firms’ performance has been established for European firms, evidence for developing countries has been mixed.9 Similar studies exist only for a subset of transition countries. Indeed, for many of them, the data required for such analysis have not existed until now.

A simple comparison of the average labour productivity of innovative and non-innovative firms does not point to a strong relationship between innovation and productivity. Innovative firms have higher average productivity in less than half of all countries. Differences between innovative and non-innovative firms also depend on the type of innovation. Only in Jordan are innovative firms significantly more productive than non-innovative firms across all types of innovation (see Table 2.1).

There may be reasons why the correlation observed between innovation and productivity is weaker than the true underlying impact that innovation has on productivity. For example, if poorly performing firms find themselves under greater pressure to innovate, innovation may appear to be linked to poor short-term performance, despite improving firms’ productivity in the longer run.

In order to deal with such issues appropriately, we need a more comprehensive analysis of the relationship between innovation and firms’ productivity that accounts for factors that may affect both firms’ productivity and the decision to innovate. To this end, this chapter uses a well-known model devised by Crépon, Duguet and Mairesse (known as the “CDM model” – see Chart 2.1.1) that links R&D, innovation and labour productivity.10 The model controls for other factors that can affect R&D, innovation and labour productivity, such as a firm’s size and age, the skills of the workforce, the level of competition and the type of industry (see Box 2.1 for details).

Once these factors are taken into account, the impact that innovation has on productivity becomes stronger.11 Product innovation is associated with a 43 per cent increase in labour productivity, and this effect has a high degree of statistical significance. This suggests that a firm with median labour productivity would move from the 50th to the 60th percentile of the labour productivity distribution after introducing a new product. Labour productivity also benefits from the implementation of process innovations. Although this effect is smaller (with the introduction of new processes being associated with a 20 per cent increase in labour productivity), it is also statistically significant. A firm with median labour productivity would move from the 50th to the 55th percentile of the labour productivity distribution after introducing a new process. These effects are somewhat stronger than those found for developed economies, but they are comparable to those observed in developing economies.12

Interestingly, the increase in labour productivity is smaller for firms that engage in product and process innovation simultaneously than it is for those that engage exclusively in either product or process innovation. This can be explained by the fact that simultaneous product and process innovation is more complex and takes longer to be fully reflected in increased labour productivity, while BEEPS data only enable us to look at the short-term impact of new products and processes.

The estimated effects are stronger when using self-reported measures of innovation than when using cleaned measures. In the case of product innovation, the estimated improvement in productivity is 69 per cent when a self-reported measure of innovation is used, compared with a 43 per cent improvement when using a cleaned measure. This could be because almost a quarter of all self-reported product innovations and 11 per cent of all self-reported process innovations were in fact either organisational or marketing innovations (see Box 1.1), which nevertheless result in increased turnover per worker. Indeed, the increase in labour productivity associated with self-reported organisational and/or marketing innovation is estimated at 67 per cent.13 Organisational and marketing innovations are probably less risky and costly for firms than technological innovations and, given these high productivity yields, it is perhaps surprising that less than a third of all BEEPS firms engage in either. This could be due to a lack of information on new organisational and marketing methods, scepticism regarding their effectiveness or resistance to change within organisations.14

| Level of significance | |||

|---|---|---|---|

|

Type of innovative activity |

1% |

5% |

10% |

|

R&D |

Jordan, Moldova, Romania, Russia |

Armenia, Croatia, |

Uzbekistan |

|

Product and process |

Jordan |

Kyrgyz Rep., Moldova, Mongolia |

Armenia, FYR Macedonia, Uzbekistan |

|

Organisational and marketing (self-reported) |

Belarus, Jordan, Latvia, Russia, Slovenia |

Kyrgyz Rep., Lithuania, Mongolia, Romania, Tajikistan, Turkey |

Kazakhstan, Montenegro |

|

Product and process (cleaned) |

Jordan, Moldova, Mongolia, Ukraine |

||

Source: BEEPS V, MENA ES and authors’ calculations.

Note: There are no BEEPS firms engaged in research and development (R&D) in Azerbaijan. Cleaned data on product and process innovation were not available for the Slovak Republic, Tajikistan or Turkey at the time of writing.

| Associated impact on firm-level productivity | ||

|---|---|---|

| (1) | (2) | |

| Type of innovation | Cleaned | Self-reported |

|

Product innovation |

0.355*** |

0.524*** |

|

(0.024) |

(0.032) |

|

|

Process innovation |

0.179*** |

0.256*** |

|

(0.021) |

(0.021) |

|

|

Product or process innovation |

0.227*** |

0.448*** |

|

(0.024) |

(0.028) |

|

|

Non-technical innovation |

0.511*** |

|

Source: BEEPS V, MENA ES and authors’ calculations.

Note: This table reports regression coefficients for the occurrence of innovation at firm level, reflecting the impact on the dependent variable firm-level productivity, which is measured as turnover (in US dollars) per employee in log terms. The results are obtained by estimating a three-stage CDM model by asymptotic least squares (ALS), where productivity is linked to innovation, and innovation, in turn, is related to investment in R&D. For a detailed description and the set of control variables included, refer to Box 2.1. Standard errors are reported in parentheses below the coefficient. ***, ** and * denote statistical significance at the 1, 5 and 10 per cent levels respectively.

In which sectors does innovation boost labour productivity most? Chapter 1 showed that product innovation is more prevalent in high-tech manufacturing sectors and knowledge-intensive services. However, these are not necessarily the sectors with the largest returns to innovation (see Chart 2.2).

On the contrary, returns to product innovation are particularly large for firms in low-tech manufacturing sectors (such as food products or textiles), where introducing a new product typically results in labour productivity more than doubling (for an example of an innovative firm in the food sector in Romania, see Case study 2.1). In medium-low-tech manufacturing sectors (such as plastic products and basic metals)15, introducing a new product is associated with a 126 per cent increase in labour productivity, while in high-tech and medium-high-tech (“higher-tech”) manufacturing sectors (such as machinery and equipment or chemicals) the average increase is 91 per cent.16

These effects are fairly sizeable, but they are not as large when placed in the context of the labour productivity distribution. A low-tech manufacturing firm with median labour productivity would move from the 50th to the 82nd percentile of the labour productivity distribution after introducing a new product. A higher-tech manufacturing firm, on the other hand, would move from the 50th to the 69th percentile of the labour productivity distribution.17

This variation in estimated returns to innovation can be explained by differences in the probability of introducing new products and the level of competitive pressures faced. Firms in high-tech manufacturing sectors are more likely to introduce new products (see Chart 2.3) and more likely to compete in national or international markets (as opposed to local markets). While these competitive pressures may explain why firms have greater incentives to introduce new products, they may also limit returns to innovation because such firms tend to be fairly productive in the first place. In low-tech manufacturing sectors, on the other hand, most innovations come from suppliers of equipment and materials,18 so low-tech firms’ ability to innovate depends crucially on their ability to adapt their production processes and the adaptability of their employees.19 The relatively small number of firms that manage to adapt and introduce new products successfully may manage to capture a larger market share as a result of their innovations, thereby increasing their output per worker. Some innovations by firms in low-tech manufacturing sectors may be due to firms moving production from China to eastern Europe owing to rising wage costs in China and the increasing cost of fossil fuels.20

Sam Mills is an interesting case – an agribusiness company which has managed to significantly increase the value added by its products through substantial R&D activities.

Sam Mills is a Romanian group specialising in corn processing, corn-based food ingredients and, more recently, snacks and gluten-free products. The group’s first company was founded in 1994 and focused on corn milling. Sam Mills has grown over the years and now comprises a total of 10 companies with a wide range of activities, including the production and distribution of many different corn and pasta products.

Substantial investment in R&D activities since the mid-2000s has enabled the group to develop higher-value-added products such as feed, corn-based food ingredients and, more recently, healthy snacks and food products (mainly gluten-free pasta, cereals and products with a low glycaemic index). As a result, the group is one of the few companies in Romania that sells products through established retail chains in the United States, the EU and Asia (including chains such as Walmart, Wegmans and Delhaize), as well as selling products via Amazon and in specialist health food stores.

Source: BEEPS V, MENA ES and authors’ calculations.

Note: This chart reports the impact of innovation at firm level by sector, reflecting the impact on the dependent variable firm-level productivity, which is measured as turnover (in US dollars) per employee. The results are obtained by estimating a three-stage CDM model by ALS, where productivity is linked to innovation, and innovation, in turn, is related to investment in R&D. For a detailed description and the set of control variables included, refer to Box 2.1. The baseline model is adjusted slightly to account for the smaller sample size resulting from regressions on sector subsamples. State ownership variables are not included, as there are too few observations in some regions; the use of email is not included when explaining the incidence of R&D, as in some regions all firms make use of email. A robustness check on the baseline regression in Table 2.2 indicates that the main results remain valid after applying these adjustments. All coefficients associated with the impacts shown are statistically significant at the 1 per cent level. Sectors are based on ISIC Rev. 3.1. High-tech and medium-high-tech manufacturing sectors include chemicals (24), machinery and equipment (29), electrical and optical equipment (30-33) and transport equipment (34-35, excluding 35.1). Low-tech manufacturing sectors include food products, beverages and tobacco (15-16), textiles (17-18), leather (19), wood (20), paper, publishing and printing (21-22) and other manufacturing (36-37). Knowledge-intensive services include water and air transport (61-62), telecommunications (64) and real estate, renting and business activities (70-74).

Source: BEEPS V, MENA ES, Chart 2.2 and authors’ calculations.

Note: For definitions of sectors, see the note accompanying Chart 2.2.

Besides innovation, there are other ways of improving firm-level labour productivity. Firms can make better use of their excess capacity (provided there is any) or improve their management practices. BEEPS V offers valuable insight into the role of these factors in manufacturing firms.21

Recent studies show that there is a strong correlation between the quality of management practices and firms’ performance, and this also applies to transition countries and other emerging markets. Furthermore, a lack of managerial skills is one explanation for the low productivity of state-owned and formerly state-owned firms.22

In a management field experiment looking at large Indian textile firms, improved management practices resulted in a 17 per cent increase in productivity in the first year through improvements in the quality of products, increased efficiency and reduced inventories.23 This suggests that improving management practices may be a relatively low-cost and low-risk way of boosting firms’ productivity across the transition region.

BEEPS V includes a subset of questions on management practices taken from the Management, Organisation and Innovation (MOI) survey conducted by the EBRD and the World Bank.24 These questions look at core management practices relating to operations, monitoring, targets and incentives. They range from dealing with machinery breakdowns to factors determining the remuneration of workers. On the basis of firms’ answers, the quality of their management practices can be assessed and given a rating, which can then be used to explain productivity levels (see Box 2.2 for details).

Estimates suggest that improving the average firm’s management practices from the median to the top 12 per cent is associated with a 12 per cent increase in labour productivity, everything else being equal (see Table 2.3). The estimated impact on productivity is larger still when process innovation is also accounted for (standing at 19 per cent). Despite these sizeable effects, estimated returns to better management practices tend to be somewhat lower than returns to innovation, regardless of the type of innovation.

There are significant differences across regions in terms of the role played by improved management practices in boosting firms’ productivity. In EU member states, candidate countries and potential candidate countries (in other words, the CEB and SEE regions), where the quality of management practices tends to be higher, returns to further improvements in management practices are lower than returns to process innovation (see Chart 2.4). In the SEE region, process innovation is associated with an increase in labour productivity of more than 150 per cent. This may be largely due to the upgrading of production facilities with the aim of being more competitive in the EU market.

On the other hand, in less developed countries, where the quality of management is generally lower, returns to better management practices are much higher than returns to process innovation. In the EEC region, for example, better management practices are associated with a 40 per cent increase in labour productivity, whereas the introduction of a new process is associated with a mere 6 per cent increase. In Russia returns to better management and process innovations are estimated at 32 and 2 per cent respectively.

These findings raise the question of why firms in these regions (and less developed countries more generally) do not adopt better management practices. The recent management field experiment looking at large Indian textile firms suggests that this may be due to information barriers. Firms might not have heard of some management practices, or they may be sceptical regarding their impact.25 Improvements to certain management practices – particularly those relating to underperforming employees, pay or promotions – may also be hampered by regulations or a lack of competition (since competition could force badly managed firms to exit the market).

Training programmes covering basic operations (such as inventory management and quality control) could be helpful, but suitable consultancy or training services offering such products may not exist in a given market or may be geared towards large firms, making them too expensive for SMEs.26

The EBRD’s Business Advisory Services (BAS) and Enterprise Growth Programme (EGP) promote good management practices in micro, small and medium-sized enterprises (MSMEs) in the transition region, providing direct support to individual enterprises.27 Box 3.4 analyses links between the use of consultancy services, innovation, management practices and productivity in the transition region.

| Log of labour productivity | ||||

|---|---|---|---|---|

|

Product innovation (cleaned)

|

0.575*** |

|||

|

(0.073) |

||||

|

Process innovation (cleaned)

|

0.178*** |

|||

|

(0.062) |

||||

|

Product or process innovation (cleaned)

|

0.415*** |

|||

|

(0.073) |

||||

|

Non-technical innovation |

0.226*** |

|||

|

(0.059) |

||||

|

Management quality

|

0.115*** |

0.176*** |

0.132*** |

0.135*** |

|

(0.037) |

(0.037) |

(0.037) |

(0.037) |

|

|

Capacity utilisation

|

0.004** |

0.003* |

0.004** |

0.007*** |

|

(0.002) |

(0.002) |

(0.002) |

(0.002) |

|

|

Log of fixed assets per employee

|

0.178*** |

0.191*** |

0.179*** |

0.197*** |

|

(0.015) |

(0.015) |

(0.015) |

(0.015) |

|

Source: BEEPS V, MENA ES and authors’ calculations.

Note: This table reports regression coefficients for firm-level innovation, management quality, capacity utilisation and capital intensity in the manufacturing sector, reflecting the impact on the dependent variable firm-level productivity, which is measured as turnover (in US dollars) per employee in log terms. The results are obtained by estimating a three-stage CDM model by ALS, where productivity is linked to innovation, and innovation, in turn, is related to investment in R&D. For a detailed description and the set of control variables included, refer to Box 2.1. Standard errors are reported in parentheses below the coefficient. ***, ** and * denote statistical significance at the 1, 5 and 10 per cent levels respectively.

Source: BEEPS V, MENA ES and authors’ calculations.

Note: This chart reports the impact of firm-level process innovation and firms’ management quality by region, reflecting the impact on firm-level productivity, which is measured as turnover (in US dollars) per employee in log terms. The results are obtained by estimating a three-stage CDM model by ALS, where productivity is linked to innovation, and innovation, in turn, is related to investment in R&D. For a detailed description and the set of control variables included, refer to Box 2.1. The reported coefficients for process innovation are significant at the 1 per cent level in the CEB region, the SEE region and Russia, and at the 5 per cent level in the EEC region. The reported coefficients for management scores are significant at the 1 per cent level in the EEC region and Russia, and at the 5 per cent level in Central Asia. Other reported coefficients are not significantly different from zero.

In addition to innovation and the quality of management, other factors do of course also affect labour productivity. Analysis shows that higher levels of capacity utilisation and greater capital intensity (in other words, capital per worker) are typically associated with higher levels of productivity.28 Firms that are located in a country’s capital or main business centre tend to be more productive, as they have access to better supporting infrastructure and a larger pool of skilled labour. Skilled labour is itself an important factor, as firms in which a higher percentage of employees are university graduates tend to be more productive.

The results also confirm that higher levels of competition – particularly competition with foreign firms – can put pressure on firms to improve productivity. Our analysis confirms that BEEPS firms that sell primarily in national or international markets are more productive than firms that primarily target local markets. There is also evidence that majority foreign-owned firms tend to be more productive. The effects of economic openness and firms’ integration into global production chains are discussed in more detail in Boxes 2.3 and 3.2.

The relationship between innovation and productivity may also be dependent on the business environment in which firms operate. Business environments are predominantly a country-level characteristic, with some variation across industries and regions within an individual country. Thus, in firm-level analysis they are typically subsumed within “fixed effects” in regressions. In order to see how business environments and innovation may combine to affect growth, the next section makes use of cross-country data.

Examining the relationship between innovation and economic performance at the country level poses its own challenges, as many factors will affect a country’s growth and, at the same time, be related to the country’s ability to innovate. In an effort to overcome this problem, the analysis below focuses on the performance of individual industries. It seeks to explain differences between the average rates of export growth of industries with different levels of innovation intensity (as defined in Chapter 1) across various countries over the period 1990-2010.29

The growth rates of industries’ exports can be affected by a number of country-level characteristics (such as macroeconomic conditions or political stability), as well as a number of industry-level characteristics. For instance, industries which cater for consumer demand in emerging markets may grow faster.

In addition, certain industries may grow faster in countries with specific characteristics. In particular, better economic institutions may enable the exports of innovation-intensive industries to grow more rapidly.

Indeed, poor economic institutions – high incidence of corruption, weak rule of law, burdensome red tape, and so on – can substantially increase the cost of introducing new products and greatly increase the uncertainty of returns to investment in new products and technologies. As a result, risk-adjusted returns to innovation may look less attractive when economic institutions are weak. This will primarily affect industries where the introduction of new products and technologies is essential in order to maintain the competitiveness of exports, so firms tend to introduce new products more frequently – in other words, innovation-intensive industries.

The BEEPS results provide some support for this view. Firms that have introduced a new product in the last three years regard all aspects of their immediate business environment as a greater constraint on their operations than firms that do not innovate. Such differences between innovative and non-innovative firms’ perception of their business environment are particularly large when it comes to the skills of the workforce, corruption and customs and trade regulations (as discussed in more detail in Chapter 3).

In order to examine the relationship between the quality of economic institutions and the growth of innovative industries, we can look at growth rates for the exports of various industries in various countries.30 These can be explained by country fixed effects (roughly corresponding to the average growth rates of total exports in individual countries) and industry fixed effects (namely the average growth rates of global exports for individual industries), as well as the initial exports of a given industry in a given country, expressed as a percentage of that country’s total goods exports. In addition, regressions include interaction terms between the innovation intensity of a given industry and a country-level characteristic: either the quality of economic institutions or the level of financial development. A positive and significant coefficient for the interaction term between innovation intensity and the quality of economic institutions would imply that innovation-intensive exports grow relatively fast compared with other exports in countries that have superior economic institutions.

The quality of economic institutions is measured using the average of four of the World Bank’s Worldwide See Kaufmann et al. (2009) for a discussion.”]31[/tooltip] These indicators range from -2.5 to 2.5, with higher values corresponding to stronger underlying economic institutions. Financial development is captured by the ratio of private-sector credit to GDP (as reported in the World Bank’s Global Financial Development Database)32 and primarily reflects the level of development of banking services. In order to see whether these same factors influence the incidence of innovation in advanced economies and emerging/developing economies, the relevant coefficients were allowed to vary between the two groups of countries.33

The results are presented in Table 2.4. They suggest that the exports of innovation-intensive industries do grow faster relative to other exports in countries with stronger economic institutions and that this effect is statistically significant. These estimates also indicate that the impact the quality of institutions has on the relative performance of innovation-intensive exports is greater in emerging/developing economies than it is in advanced economies (where the quality of economic institutions tends to be higher).

In order to understand the magnitude of this effect, we can look at one industry which is in the top 25 per cent in terms of innovation intensity (for instance, pharmaceuticals) and another which is in the bottom 25 per cent (such as basic metals). A 1-standard-deviation improvement in the quality of economic institutions (say, from the level of Albania to that of Poland) will boost the average growth rate of the exports of the more innovation-intensive industry, pharmaceuticals, by an extra 0.35 percentage point a year relative to the growth rate of basic metals. In the case of emerging markets, the extra growth premium for the more innovation-intensive industry stands at 0.95 percentage point a year. This is a sizeable difference, given that the median rate of growth across all industries and countries in the sample is around 8 per cent.

The specifications reported in columns 3 and 4 suggest a similar relationship with financial development, with the exports of innovation-intensive industries also growing faster relative to other exports in countries with higher credit-to-GDP ratios. This reflects the fact that industries that are more innovation-intensive may be more reliant on the availability of credit in order to fund investment in the development of new products (as discussed in more detail in Chapter 4 of this report).

| [1] | [2] | [3] | [4] | |

|---|---|---|---|---|

| Dependent variable | Industry’s average annual export growth, 1990-2010 (per cent) | |||

|

Industry’s share in |

-0.176*** |

-0.175*** |

-0.175*** |

-0.175*** |

|

(0.020) |

(0.020) |

(0.021) |

(0.021) |

|

|

Innovation intensity * |

0.008*** |

|||

|

(0.0030) |

||||

|

Innovation intensity * |

0.013*** |

|||

|

(0.004) |

||||

|

Innovation intensity * |

0.022*** |

|||

|

(0.006) |

||||

|

Innovation intensity * |

0.007** |

|||

|

(0.004) |

||||

|

Innovation intensity * |

0.010** |

|||

|

(0.004) |

||||

|

Innovation intensity * |

0.013** |

|||

|

(0.006) |

||||

|

Industry fixed effects |

Yes |

Yes |

Yes |

Yes |

|

Country fixed effects |

Yes |

Yes |

Yes |

Yes |

|

Number of observations |

3,069 |

3,069 |

3,001 |

3,001 |

|

Number of countries |

144 |

144 |

140 |

140 |

|

R2 |

0.501 |

0.503 |

0.500 |

0.500 |

Source: Authors’ calculations using data from UN Comtrade and Feenstra et al. (2005) (exports data), US Bureau of Labor Statistics (deflators, employment), USPTO (US patent grants), and the World Bank’s Worldwide Governance Indicators (ratio of private-sector credit to GDP).

Note: The dependent variable is average annual growth in exports for a given industry in a given country between 1990 and 2010. Export values have been deflated using industry-specific deflators calculated for US industries. As the United States is used to estimate the innovation intensity of industries, it is excluded from all regressions. All regressions include country and industry fixed effects. Data on Worldwide Governance Indicators are averages for the period 1996-2010; data on the ratio of private-sector credit to GDP are averages for the period 1990-2010. Robust standard errors are indicated in parentheses. ***, ** and * denote statistical significance at the 1, 5 and 10 per cent levels respectively.

All in all, there are large differences in labour productivity across both firms and countries in the transition region. Every transition country has firms with high and low labour productivity. However, in less developed transition countries the percentage of firms with poor productivity is higher.

How can firms boost their productivity? Analysis suggests that all types of innovation – product, process, marketing and organisational innovation – play an important role. Moreover, even if they do not advance the technological frontier, innovations which are new to an individual firm can still result in large productivity dividends. Returns to innovation are particularly high in low-tech manufacturing sectors, where innovation is less common.

Another important source of labour productivity gains is improvements in the quality of management. In less developed transition countries, where the quality of management is generally poor, returns to improvements in management are high, while returns to process innovation are generally low.This suggests that management practices need to be improved before new processes can lead to sizeable productivity gains. In contrast, in the CEB and SEE regions, where management practices tend to be better, returns to the introduction of new processes exceed returns to further improvements in management.

Cross-country analysis of the exports of various industries suggests that industries involving higher levels of innovation are able to grow faster, thereby driving overall economic growth – provided that the business environment is accommodative. These estimates also imply that the quality of the business environment is particularly important for the development of innovation-intensive industries. The results suggest that improvements in the quality of economic institutions are associated with increases in the innovation intensity of exports and output over time as innovation-intensive industries grow faster and their relative contribution to the country’s exports rises. Chapter 3 examines the relationship between the quality of the business environment and firm-level innovation in more detail.

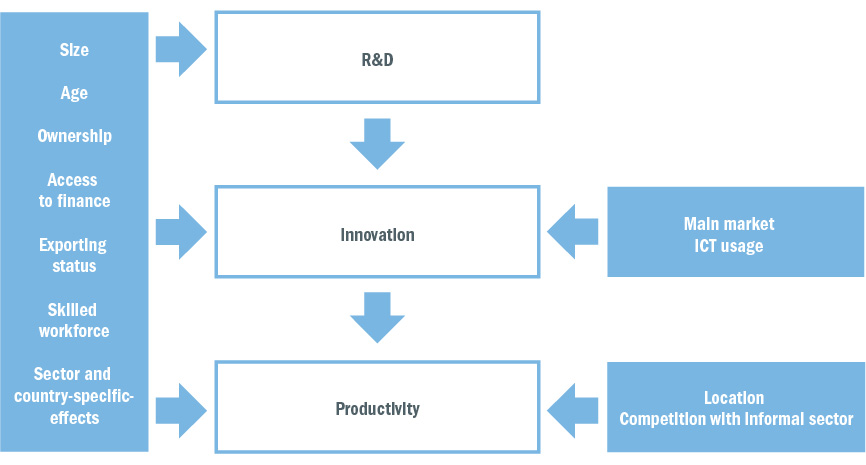

The impact that innovation has on productivity is estimated here using a well-established three-stage model which links productivity to firms’ innovation activities and, in turn, treats innovation as an outcome of firms’ investment in R&D.34 This three-stage structure (explaining: (i) the decision to engage in R&D; (ii) the decision to introduce a new product or process; and (iii) the firm’s labour productivity) is used because the management’s decisions to invest in R&D and develop/introduce innovations are likely to influence each other. In addition, these processes often take place simultaneously (see Chart 2.1.1).35

As a result, all stages are estimated simultaneously in order to address the endogeneity bias, using an asymptotic least squares (ALS) estimator and the BEEPS V and MENA ES datasets. The first stage estimates the innovation input equation:

This represents the probability of R&D investment being conducted by firm i , where R&Di takes the value of 1 whenever the latent value of R&D reported by the firm, R&Di*, is larger than zero. Xi1 is a vector of variables explaining the occurrence of R&D investment, including the firm’s size, age, direct exporter status, percentage of employees with a completed university degree, and ownership structure (whether the majority of the firm is owned by a foreign company or the state), and the percentages of working capital and fixed assets that are financed by bank loans or loans from non-bank financial institutions (NBFIs). To account for sector and country-specific differences in firm-level investment in R&D, sector and country fixed effects are included. This set of variables is assumed to influence not only R&D investment, but also productivity and innovation, as shown in Chart 2.1.1.

The second stage of the model determines the probability of a firm implementing innovation, taking into account its investment in R&D. The latent variable R&Di* which was derived from the first stage is used to explain the impact that R&D investment has on innovative activities. This solves the aforementioned problem of the endogeneity bias:

In this equation, the coefficient γ denotes the impact that R&D investment has on the probability of a firm introducing an innovation (as discussed in more detail in Chapter 3). Innovationi refers to the occurrence of the various types of innovation introduced in Chapter 1. The probability of observing such an innovation is explained by the vector Xi2 , which includes the set of variables that were introduced in the first stage, plus measures reflecting the firm’s level of geographical expansion (that is to say, whether the firm’s main product is mostly sold in the local market) and the firm’s level of ICT use (in other words, whether it uses email to communicate with its clients; see Chart 2.1.1).

The final stage of the model relates the firm’s innovative activities – explained by its investment in R&D – to labour productivity (measured as turnover per employee, converted into US dollars, in log terms), again using the latent inferred variable to explain differences across firms with regard to productivity:

In this chapter, the focus is on the coefficient ξ, which reflects the impact that innovation has on labour productivity. In addition to the set of control variables used in the first and second stages, vector Xi3 , which is used to explain variations in productivity, includes information on whether the firm is located in the country’s capital or main business centre, and whether the firm competes with unregistered or informal firms (see Chart 2.1.1).

Source: Authors’ representation of the model.

Note: Based on Crépon et al. (1998).

BEEPS V and MENA ES included a section on management practices in the areas of operations, monitoring, targets and incentives. The operations question focused on how the firm handled a process-related problem, such as machinery breaking down. The monitoring question covered the collection of information on production indicators. The questions on targets focused on the timescale for production targets, as well as their difficulty and the awareness of them. Lastly, the incentives questions covered criteria governing promotion, practices for addressing poor performance by employees and the basis on which the achievement of production targets was rewarded. These questions were answered by all manufacturing firms with at least 20 employees (at least 50 employees in the case of Russia). The median number of completed interviews with sufficiently high response rates was just below 55 per country, with totals ranging from 15 in Montenegro to 626 in Turkey.36

The scores for individual management practices (in other words, for individual questions) were converted into z-scores by normalising each practice so that the mean was 0 and the standard deviation was 1. To avoid putting too much emphasis on targets or incentives, unweighted averages were first calculated using the z-scores of individual areas of the four management practices. An unweighted average was then taken across the z-scores for the four practices. Lastly, a z-score of the measure obtained was calculated. This means that the average management score across all firms in all countries in the sample is equal to zero, with the management practices of individual firms deviating either left or right from zero, with the former denoting bad practices and the latter indicating good practices.

There is a significant positive correlation between average labour productivity and the average quality of management practices (see Chart 2.2.1). As with labour productivity, there are firms with good and bad management practices in all countries. However, countries where the average quality of management is lower have a smaller percentage of firms with good management practices than countries where the quality of management tends to be higher.

Source: BEEPS V, MENA ES and authors’ calculations.

Competitiveness can be understood as a country’s ability to sell its products in the global market, so it has traditionally been measured as a country’s gross share of export markets. However, over the past two decades the world has witnessed rapid cross-border integration of production networks. This deep global integration means that analysis of a country’s gross export market share may result in misleading conclusions, since it does not account for the domestic share of value added in products. For example, if a particular export good contains many imported intermediate goods, the domestic share of value added will be small and gross export flows will say little about the country’s true competitiveness.

To provide an accurate picture of competitiveness trends across the transition region, this box uses a methodology proposed by Benkovskis and Wörz37 to account for changes in the value-added content of trade. It combines a theoretically consistent breakdown of changes in export market shares with highly disaggregated trade data from UN Comtrade and information from the World Input-Output Database. This allows the traditional approach to measuring a country’s competitiveness (that is to say, changes in gross export market shares) to be compared with a value-added approach (in other words, changes in a country’s value added content in its gross export market share).

Both approaches allow changes in competitiveness to be broken down into two main components: the extensive margin of trade (in other words, changes that are due to new products or markets) and the intensive margin (that is to say, export growth in existing markets). In turn, the contribution made by the intensive margin can be broken down into four elements: price factors (such as the exchange rate); non-price factors (such as quality and taste); shifts in the structure of global demand (triggered, for instance, by shifts in preferences for individual products); and changes in the set of competitors (for instance, the emergence of new suppliers providing identical or similar products). The value-added approach introduces a new component that captures the role played by a country’s integration into global production chains.

The diamonds in Charts 2.3.1 and 2.3.2 indicate cumulative changes in selected transition countries’ global market shares for final goods in the period 1996-2011. The two charts paint a similar picture in terms of the growth of market shares. Bulgaria, Hungary, Poland, Romania, Slovak Republic and Turkey all increased their market shares, while Slovenia saw its global competitiveness decline. Thus, the trend in these countries was similar to that observed in other emerging economies, such as Brazil, China and India, which saw their global market shares rise overall during this period.

The new breakdown described in this box reveals that the underlying determinants of increases in global competitiveness are very different when the focus shifts to value added. For a number of countries (including Bulgaria, Hungary, Poland, Romania and Russia), the contributions made by price and non-price factors are the opposite of what one would see using traditional statistics. As in other emerging markets, traditional trade statistics overestimate improvements in the quality of exported products in the transition region.

The traditional approach suggests that improvements in non-price competitiveness have led to increases in market shares, while price developments have curbed competitiveness. A decline in the price competitiveness of Romania, for instance, means that, overall, the price of products that it exports in a given market has increased relative to the price of identical products sold by its competitors. Rising non-price competitiveness, on the other hand, could mean that the quality of products exported by Romania has increased overall relative to the average quality of identical products exported by other providers.

The new breakdown reveals that the price competitiveness of transition economies has in fact increased, while the contribution made by non-price factors has declined considerably (even becoming negative in the case of Poland). For instance, an increase in the price of products sold by Romania (a decline in price competitiveness) may actually be due to an increase in the price of the inputs that it imports in order to manufacture those products, rather than being due to an increase in its own production costs. Similarly, improvements to the quality of the products exported by Romania may have been made upstream in another country (rather than being made in Romania). The new breakdown based on value added distinguishes between these different effects.

Similar results are recorded for Brazil, China and India. Non-price competitiveness showed a negative – or, in the case of China, reduced – contribution to value-added market share gains.

Thus, for all of these countries, their apparent non-price competitiveness based on their shares of gross export markets is largely the result of deeper integration into global value chains. Foreign consumers seem to attach a greater value to products from these countries because they are perceived to involve higher-quality inputs and carry better branding owing to outsourcing. In the case of Russia, this change of approach reveals an extraordinarily strong positive contribution by price competitiveness and a shift in global production chains owing to its energy-dependent export basket.

In conclusion, this box shows that transition countries have been able to increase their share of global markets thanks to their ability to participate in global production chains. Poland, Romania and the Slovak Republic have been the primary beneficiaries of this change in global production. At the same time, the cost competitiveness of firms in the transition region allows them to build on their increased market shares. These firms’ ability to maintain price competitiveness despite unit costs converging with the levels seen in western Europe is an encouraging sign. Looking ahead, however, better branding and higher-quality production will remain key for all firms – irrespective of their participation in global value chains – when it comes to increasing their shares of world markets.

Source: UN Comtrade and authors’ calculations.

Source: UN Comtrade and authors’ calculations.

J. Arnold, G. Nicoletti and S. Scarpetta (2008)

“Regulation, allocative efficiency and productivity in OECD countries: Industry and firm-level evidence”, OECD Economics Department Working Paper No. 616.

D. Atkin, A. Chaudhry, S. Chaudry, A.K. Khandelwal and E. Verhoogen (2014)

“Organizational barriers to technology adoption: Evidence from soccer-ball producers in Pakistan”, mimeo.

(last accessed on 17 August 2014).

E. Bartelsman, J.C. Haltiwanger and S. Scarpetta (2004)

“Microeconomic evidence of creative destruction in industrial and developing countries”, World Bank Policy Research Working Paper No. 3464.

T. Beck, A. Demirgüç-Kunt and R. Levine (2000)

“A new database on financial development and structure”, World Bank Economic Review, Vol. 14, No. X, pp. 597-605.

K. Benkovskis and J. Wörz (2013)

“Non-price competitiveness of exports from emerging countries”, ECB Working Paper No. 1612.

K. Benkovskis and J. Wörz (2014)

“‘Made in China’ – How does it affect measures of competitiveness?”, OeNB Working Paper No. 193.

N. Bloom and J. Van Reenen (2010)

“Why do management practices differ across firms and countries?”, Journal of Economic Perspectives, Vol. 24, No. 1, pp. 203-224.

N. Bloom, H. Schweiger and J. Van Reenen (2012)

“The land that lean manufacturing forgot? Management practices in transition countries”, Economics of Transition, Vol. 20, No. 4, pp. 593-635.

N. Bloom, B. Eifert, A. Mahajan, D. McKenzie and J. Roberts (2013)

“Does management matter? Evidence from India”, Quarterly Journal of Economics, Vol. 128, No. 1, pp. 1–51.

B.P. Bosworth and J.E. Triplett (2007)

“Services productivity in the United States: Griliches”, in E.R. Berndt and C.R. Hulten (eds.), Hard-to-Measure Goods and Services: Essays in Honor of Zvi Griliches, University of Chicago Press, pp. 413-447.

J.D. Brown, J.S. Earle and A. Telegdy (2006)

“The productivity effects of privatization: Longitudinal estimates from Hungary, Romania, Russia, and Ukraine”, Journal of Political Economy, Vol. 114, No. 1, pp. 61-99.

E. Brynjolfsson and L.M. Hitt (2000)

“Beyond computation: Information technology, organizational transformation, and business performance”, Journal of Economic Perspectives, Vol. 14, No. 4, pp. 23-48.

B. Crépon, E. Duguet and J. Mairesse (1998)

“Research, innovation and productivity: An econometric analysis at the firm level”, Economics of Innovation and New Technology, Vol. 7, No. 2, pp. 115-158.

EBRD (2009)

Transition Report 2009: Transition in Crisis?, Chapter 5, London.

S. Estrin, J. Hanousek, E. Kočenda and J. Svejnar (2009)

“The effects of privatization and ownership in transition economies”, Journal of Economic Literature, Vol. 47, No. 3, pp. 699-728.

European Commission (2014)

Industrial Innovation Policy. http://ec.europa.eu/enterprise/policies/innovation/policy/index_en.htm (last accessed on 15 August 2014).

L. Foster, J.C. Haltiwanger and C. Syverson (2008)

“Reallocation, firm turnover and efficiency: Selection on productivity or profitability?”, American Economic Review, Vol. 98, No. 1, pp. 394-425.

J. Gwartney, R. Lawson and J. Hall, with A.M. Crisp, B. Knoll, H. Pitlik and M. Rode (2013)

Economic Freedom of the World: 2013 Annual Report, Fraser Institute, Vancouver.

B.H. Hall, F. Lotti and J. Mairesse (2009)

“Innovation and productivity in SMEs: Empirical evidence for Italy”, Small Business Economics, Vol. 33, No. 1, pp. 13-33.

M. Heidenreich (2009)

“Innovation patterns and location of European low- and medium-technology industries”, Research Policy, Vol. 38, No. 3, pp. 483-494.

C.-T. Hsieh and P. Klenow (2009)

“Misallocation and manufacturing TFP in China and India”, Quarterly Journal of Economics, Vol. 124, No. 4, pp. 1403-1448.

D. Kaufmann, A. Kraay and M. Mastruzzi (2009)

“Governance matters VIII: Governance indicators for 1996-2008”, World Bank Policy Research Working Paper No. 4978.

J. Mairesse, P. Mohnen and E. Kremp (2005)

“The importance of R&D and innovation for productivity: A re-examination in light of the French Innovation Survey”, Annales d’Economie et de Statistique, No. 79/80, pp. 487-527.

D. McKenzie and C.M. Woodruff (2014)

“What are we learning from business training and entrepreneurship evaluations around the developing world?”, World Bank Research Observer, Vol. 29, No. 1, pp. 48-82.

P. Mohnen and B.H. Hall (2013)

“Innovation and productivity: An update”, Eurasian Business Review, Vol. 3, No. 1, pp. 47-65.

I. Moss (2011)

“Start-up nation: An innovation story”, OECD Observer, No. 258, Q2 2011. Available at: www.oecdobserver.org/news/printpage.php/aid/3546/Start-up_nation:_An_innovation_story.html (last accessed on 20 August 2014).

G.S. Olley and A. Pakes (1996)

“The dynamics of productivity in the telecommunications equipment industry”, Econometrica, Vol. 64, No. 6, pp. 1263-1297.

J. Raffo, S. Lhuillery and L. Miotti (2008)

“Northern and southern innovativity: a comparison across European and Latin American countries”, The European Journal of Development Research, Vol. 20, No. 2, pp. 219-239.

R.G. Rajan and L. Zingales (1998)

“Financial dependence and growth”, American Economic Review, Vol. 88, No. 3, pp. 559-586.

N. Rosenbusch, J. Brinckmann and A. Bausch (2011)

“Is innovation always beneficial? A meta-analysis of the relationship between innovation and performance in SMEs”, Journal of Business Venturing, Vol. 26, No. 4, pp. 441-457.

W. Steffen and J. Stephan (2008)

“The role of human capital and managerial skills in explaining productivity gaps between East and West”, Eastern European Economics, Vol. 46, No. 6, pp. 5-24.

A. Wendlandt (2012)

“Fashion factories move west from China”, The Globe and Mail, 6 September 2012. Available at: www.theglobeandmail.com/report-on-business/international-business/fashion-factories-move-west-from-china/article535263/ (last accessed on 28 August 2014).

World Economic Forum (2013)

The Global Competitiveness Report 2013-2014, Geneva.